The Nobel Prize in economics was awarded last week to the behavioral economist Richard Thaler. Thaler was mentored by another Nobel Prize winning economist, Daniel Kahneman.

What can you learn about investing from these two Nobel Prize winning economists? A lot!

Before we talk about Thaler’s work, we’ll start with Kahneman.

Daniel Kahneman and his late colleague, Amos Tversky, are widely regarded as pioneers in behavioral finance and economics. Their work has been popularized by Michael Lewis in books like Moneyball (later made into a movie) and The Undoing Project.

Kahneman himself published a fantastic popular book just a few years ago called Thinking Fast and Slow. It’s a must read, as far as I’m concerned.

Kahneman and Tversky were some of the first academics to conclusively demonstrate the choices we make as human beings often don’t line up with the choices that academic economists think we should make.

Their theory was called prospect theory. The big takeaway for investors from prospect theory is this: As investors, we are risk-seeking when it comes to our losses, but we are risk-averse when it comes to our gains.

What does that mean?

It means that when we’ve got losses, we’re willing to take bigger risks to try to avoid those losses. We feel like we have to recover. We want to get back to break-even, and we’re willing to do crazy things (by economists’ standards) to make that happen.

On the other hand, when we have sizable gains, we tend to want to lock-in those gains and not take any more risks. As I’ve questioned before, who do you know, that doubles up on their winners?

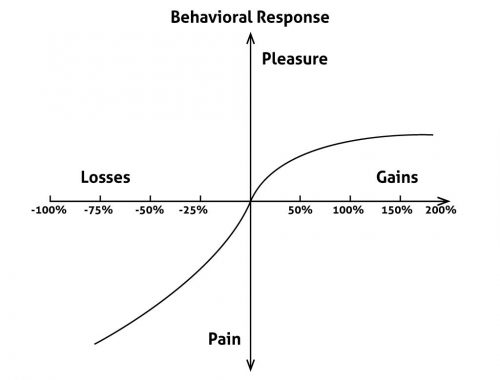

Kahneman and Tversky captured this outsized focus investors have on avoiding loss, by something they called the value function of losses and gains. It’s expressed in this simple chart:

In a nutshell, as losses increase (left side of the chart), the pain of those losses becomes much more intense. On the other hand, as gains increase, the pleasure of those gains tapers off. We just aren’t as attached to our gains as we are to our losses!

I’m personally convinced that this simple pleasure-and-pain relationship we have with gains and losses is responsible for at least half of the chronic underperformance individual investors experience in the markets. It’s what causes us to let go of our winners and hold onto our losers.

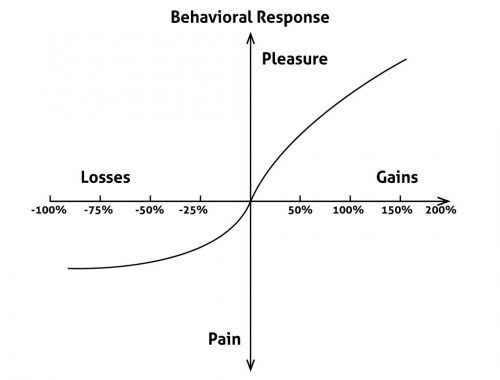

This is the reason even a simple trailing stop loss strategy, so often improves the performance of individual investors. Trailing stops, when followed with discipline, limit losses and un-limit gains! Trailing stops flip the above chart on its head, so the response to losses and gains looks like this instead:

So, that’s a lot about Kahneman and Tversky but what about Richard Thaler?

Richard Thaler made many wonderful contributions to behavioral economics. He is widely credited with being the economist who turned behavioral economics from an intellectual curiosity, into something even academic economists could respect.

He did so by proving economic models that incorporate behavioral insights, could better predict actual economic events. Thaler had better access to data and computing power than Kahneman and Tversky. That was a big advantage.

More importantly for investors, however, Thaler also expanded upon the prospect theory of Kahneman and Tversky. Thaler showed that investor behavior, when it comes to gains and losses, wasn’t quite so simplistic.

Yes, it is true that when an investor is in a big hole, he is willing to pay extra (more than he should) for the chance at getting back to “break-even.” Thaler coined this the break-even effect. I couldn’t agree more.

Thaler also showed, however, there is another situation in which we’re willing to pay more than we should be willing to pay for the chance of big gains – right after we just made a big gain already! Thaler called this the house-money effect.

When an investor has some extra money in his pocket because of a larger than expected win, he feels like he’s now playing with the “house’s money” and is free to “roll the dice” in ways he wouldn’t normally feel free to do so.

However, don’t just take it from me … take it from two Nobel Prize winning economists. Watch out for an urgent sensation, like you need to get back to “break-even,” and watch out for that euphoric “ah, what the heck” feeling that comes from playing with the house’s money.

You’ll be a much better investor for it!