Stock market bulls are feasting on a “Goldilocks Porridge” of economic data right now. Like the porridge from the famous children’s story, Goldilocks and the Three Bears, the incoming data is not too hot, and not too cold, but just right.

That makes a difference because both “too hot” and “too cold” would be a significant negative for stocks, possibly ending the bull run — but “just right” lets the run continue.

- If the data were “too hot,” that would mean rapidly accelerating growth and rising inflation pressures. In these conditions, the Federal Reserve would be forced to hike interest rates. Higher interest rates would put a brake on consumer spending and hurt corporate profits, because corporations have borrowed at low interest rates in record amounts.

- If the data were “too cold,” on the other hand, that would mean the U.S. economy is in trouble, or that corporate earnings are shrinking, or both. It would create a negative outlook for stocks in the near to medium future, with a forecast for declining profits. That would cause valuations to shrink and stock prices to fall.

We know the bulls are happy because the major indexes are at record levels and U.S. equities are having their best start to the year in decades. On April 23, the S&P 500 and Nasdaq Composite indexes broke out to new all-time highs. This officially resets the clock on any bear market concerns generated by the sharp price drop in December 2018.

It’s a historic surge. According to data from the Wall Street Journal, the S&P 500 just booked its best four-month start to the year since 1987. Meanwhile, the Nasdaq had its best four-month start since 1991, and the Dow Jones Industrial Average had its best start since 1999.

Often, though not always, an aggressive price move means investors were caught by surprise. When this happens, the power of the resulting move comes from a large group of market participants having to change their positions (e.g. money managers having to increase their bullishness and buy more stocks).

In today’s case, there have been a number of surprises all in the “Goldilocks” direction:

- Corporate earnings have been better than expected.

- Economic growth has been stronger than expected.

- Inflation pressure has been lower than expected.

- Corporate share buybacks have been stronger than expected.

Heading into the first quarter of 2019, earnings forecasts were gloomy. The consensus on Wall Street was that corporate profits would take a hit in their year-on-year comparisons, in part due to the “sugar high” of GOP tax cuts wearing off and in part due to a slowing U.S. economy.

That didn’t happen, though. Earnings season has been stronger than Wall Street analysts predicted, which has forced the investment banks to revise their forecasts upward. Credit Suisse, for example, switched from forecasting a 2.5% year-on-year earnings decline to an increase of 2.5% to 3%. That is a big swing in the Goldilocks direction.

U.S. economic growth has also been stronger than expected. Quarterly U.S. GDP (gross domestic product) just came in at 3.2%, which was high enough to catch Wall Street by surprise. There was a general belief that the U.S. economy would be slowing down more significantly by now. That isn’t the case, which is a good sign for corporate earnings.

At the same time, inflation pressures have been low. The problem with “too hot” economic growth is that it forces the Federal Reserve to raise interest rates in order to keep inflation from causing a problem. But in this particular area, U.S. economic data has been the ideal mix for stock market bulls: Strong on the outside, weak on the inside. Because inflation pressures are surprisingly low relative to bullish growth data, it is easier to see the Federal Reserve holding off on interest rate hikes.

There is even speculation that the Federal Reserve is more likely to cut interest rates again, rather than hike, when it makes its next directional move (which could be six months away or more). That would be favorable for stocks.

Last but not least, corporate share buybacks have been stronger than expected. The buyback trend has been in place for years now, but many assumed it would slow down or even peter out in 2019. Once again, that hasn’t been the case. Apple, for example, just announced plans to buy back another $75 billion worth of its own shares.

Corporate share buybacks occur when companies buy their own shares and remove them from the market. This is seen as bullish because buying pressure pushes the stock price up, a reduced supply of shares on the open market makes it easier for future buying to support the share price, and a reduced total number of shares means the earnings per share (EPS) number is higher.

There are loud debates over whether corporate share buybacks are healthy or not. Some see buybacks as a sign the company has run out of imagination. Others worry about buybacks fueled by corporate debt, as public companies sometimes borrow at low interest rates to fund their buyback programs.

Regardless of opinion, buybacks have collectively been a major bullish force when it comes to stock prices and valuations. Axios reports that U.S. companies have done $272 billion worth of buybacks in 2019, on pace to break the 2018 record of $1.085 trillion.

Some argue this whole bull market comes down to the Federal Reserve and their decision not to raise interest rates. In a way that is true. If the Federal Reserve started hiking interest rates aggressively, that would hurt corporate earnings, create a slowdown in economic growth, and possibly put an end to the buyback bonanza. It’s like a needle scratching across a record when credit conditions get tight.

But in a more important way, the Federal Reserve is not the key actor here. They are just reacting to the incoming data, which so far, has been surprisingly “Goldilocks” in nature — better than expected earnings and economic growth, but with minimal inflation pressure and the buyback trend still strong.

How long can the Goldilocks mood last? That depends on multiple factors, like the upcoming resolution of China trade talks for example. A bullish trade result — which remains likely, as it would serve both countries’ interest — could give another strong boost to investor sentiment.

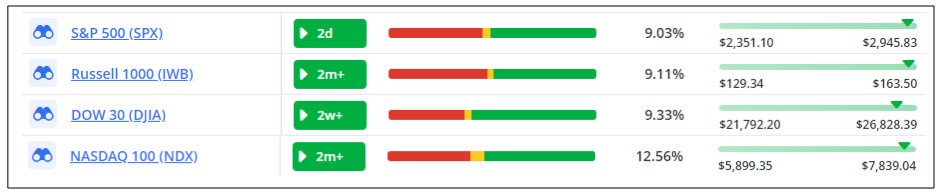

In the meantime, you can gauge the state of the major indexes via the “Market Health” area of Ideas by TradeSmith, as shown in the screenshot below.

|

The S&P 500, Russell 1,000, Dow Jones Industrial Average, and Nasdaq 100 are all in the green zone, with more components green than red, and prices at or near the high point of the past 12 months.

While the hidden drivers of the market can be complex, the outputs can be quite simple. Right now, those outputs are telling us to stay bullish and stick with the trend, as Goldilocks conditions favor more upside.