To understand the times we are in, it is helpful to know what a “Balance Sheet Recession” is, and why it is so hard to get out of one.

The Balance Sheet Recession — which can last for years, or even decades — is another crucial concept for investors to grasp, along with other concepts we’ve explained like financial repression, fiscal dominance, and the long-term debt cycle.

To recap those other terms very briefly:

- Financial repression is the process by which interest rates are kept artificially low, in order to inflate away the debt. In periods of financial repression, government bonds lose their value to inflation (which is part of the point). The Federal Reserve has committed to near-zero interest rates until 2023 — this is textbook financial repression.

- Fiscal dominance is an environment where the government is forced to spend in such large amounts, normal monetary policy is overwhelmed by the task of managing the flood of new currency and debt created by the government. With trillions in spending already on the books for 2020, and trillions more to come, we are in the early innings of a new fiscal dominance era.

- The long-term debt cycle is the natural ebb and flow of debt over a very long period of time. For multiple decades, debt, credit, and leverage are built up to ever higher levels. Once the debt load reaches its outer limit, the cycle reverses course. After that, multiple decades are spent either reducing the debt or inflating it away — and then the process starts again.

The term “Balance Sheet Recession” was introduced to the field of macroeconomics by Richard Koo, a Taiwanese-American economist, in 2003. Koo is the Chief Economist at the Nomura Research Institute in Japan.

In the early 2000s, Koo wanted to figure out the strange thing that had happened to Japan. After many years of research and contemplation of the data, the “Balance Sheet Recession” concept is what he came up with. He had to coin a new term because Japan’s post-1990 experience was new — the economics world had never seen anything like it before.

In the 1980s, Japan experienced one of the biggest equity market and real estate bubbles of all time. To give you an idea how big that bubble was, at one point the land under the Tokyo Imperial Palace — an area roughly one-quarter the size of San Francisco’s Golden Gate Park — was worth more than all the real estate in California.

In 1990, the Japan bubble burst in spectacular fashion. Thirty years later in 2020, the Nikkei 225 Index (Japan’s version of the S&P 500) is still 40% below its 1990 highs.

The Japanese economy struggled all throughout the 1990s. All attempts to revive the economy seemed to fail. And so, in 1999, the Bank of Japan (BOJ) took the wild step of introducing zero-interest-rate policy, or “ZIRP” for short. Then, in 2001, the BOJ introduced Quantitative Easing, or “QE.”

Today the world is all too familiar with ZIRP and QE. But in the 1999-2001 period, these actions were bizarre and completely new. What would happen when interest rates went to zero? What would happen when the central bank started buying bonds en masse? Nobody knew.

As it turns out, nothing much happened at all. The introduction of ZIRP and QE did not revive Japan’s economy. If anything, it might have made things worse.

Koo wanted to figure out why this was so. He asked himself, “How in the world can there be no economic growth when Japanese companies have the ability to borrow at 0% interest rates?”

What Koo realized is that corporate balance sheets were the problem. As a result of Japan’s great 1980 bubble, and the 1990s bust, Japanese corporations had a massive overhang of debt on their balance sheets. Because of that overhang, the Japanese private sector was focused on paying down the debt, and didn’t want to borrow any more — even with interest rates at zero.

Think of a household, or a business, that still has money coming in the door, but also has a gigantic debt burden to deal with. Instead of investing the extra cash flow for growth, it is likely the cash will go toward paying down debt.

When the entire private sector of a nation’s economy is oriented to paying down debt — not in terms of every single company, but aggregate saving rather than spending on the whole — it becomes almost impossible to make the economy grow.

Koo coined the term “Balance Sheet Recession” to describe what happened to Japan. There was so much debt on the books, the private sector in aggregate did not want to borrow and spend for growth. They were too busy paying off the debt that already existed.

As a result of that condition, Japan’s economy got stuck in the mud. When the BOJ tried to get things going by implementing ZIRP and then QE, nothing happened — because ZIRP and QE were not helpful in solving the Balance Sheet Recession problem.

Unlike normal recessions, which typically come and go in the course of a year or two, Balance Sheet Recessions can stretch on and on, and sometimes last for decades. They can last for as long as it takes the private sector to work off a large overhang of debt, as such that companies on the whole start borrowing and spending for growth again.

To be clear, there will always be a handful of companies borrowing and spending for growth at any given time. But macroeconomics deals with whole-economy impacts, which are determined by the net effect of what all the companies are doing as a group.

If a few companies are borrowing and spending, but the vast majority of companies are hunkered down, the net result is that the economy shrinks or flatlines rather than grows. That is what happened to Japan. It is a Balance Sheet Recession because debt-burdened balance sheets are the problem: That debt has to be worked off or dealt with.

For a number of years, the Balance Sheet Recession was a Japan-only phenomenon. There wasn’t any academic literature on the subject, because the phenomenon was too new and isolated.

As Koo pointed out, no economist was taught this stuff in their university courses, because nobody had ever seen interest rates at zero, and companies refused to borrow at rates near zero, prior to Japan’s introduction of ZIRP and QE.

After the 2008 global financial crisis, the United States and Europe entered Balance Sheet Recessions, too. While some U.S. companies continued to borrow — like publicly traded blue chips using cheap funding to buy back shares — the private sector on the whole saw its net borrowing levels shrink.

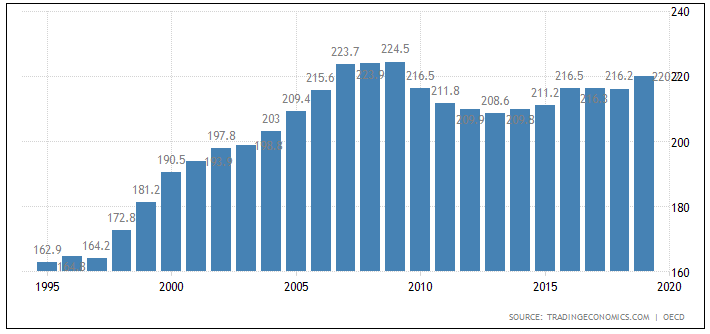

The chart below, from TradingEconomics.com, shows U.S. private sector debt to GDP dating back to 1995. As you can see from the chart, aggregate debt levels rose almost every year from the mid-1990s onward. Then, in the 2007-2009 period — when the global financial crisis unfolded — the lever was thrown into reverse.

The Balance Sheet Recession phenomenon is also worse than it appears, because so much of the borrowing done post-2009 was done for the purpose of share buybacks.

When companies borrow money to buy back shares, they artificially increase their earnings per share estimates (so the same amount of earnings is spread over a smaller number of shares). This helps the stock price go up, but it doesn’t actually increase profits, or employ more workers, or result in a positive economic impact.

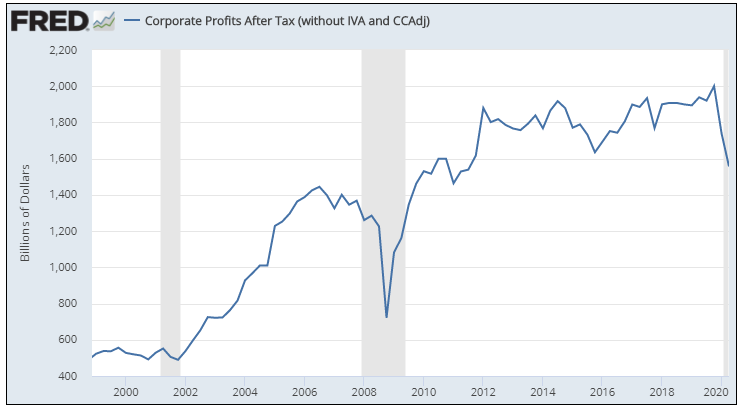

The chart below, via the St. Louis Federal Reserve, shows U.S. corporate profits after tax, on a quarterly reporting basis, since 1999. As you can see from the chart, corporate profit growth saw an impressive rebound after the global financial crisis, but then started to flatline around 2012 or so.

The years of sideways profit growth that occurred from 2012 onward are consistent with a Balance Sheet Recession. Stock prices were going up at this time, and companies were borrowing somewhat, but again, a lot of that was financial engineering — using share buybacks to juice corporate earnings.

For the U.S. to get out of its Balance Sheet Recession — and Europe, too, for that matter — the private sector will have to dig out from under the load of debt that still weighs heavily on its balance sheets.

And remember, we aren’t talking about the cash-rich tech juggernauts here, or the handful of S&P 500 companies that are making money hand over fist. We are talking about the private sector on the whole, which includes millions of struggling small businesses. (Small- and medium-sized businesses, not giant corporations, are historically the engine of job growth in the United States.)

So what about all of that zero interest rate policy (ZIRP) and quantitative easing (QE) that the Federal Reserve and European Central Bank (ECB) and Bank of England (BOE) engaged in for years, following Japan’s lead after 2008? Did QE and ZIRP help the situation any?

Unfortunately, no. According to Koo — and we agree with this — QE and ZIRP probably made the situation worse. This also goes for Europe, where they actually tried negative interest rates — an absolutely terrible idea, because it destroys the outlook for banks while doing nothing to solve the problem (too much private sector debt).

There are multiple reasons for this apart from the big one that, in a Balance Sheet Recession, trying to force-feed loans to the private sector at 0% interest rates doesn’t work. If there is no net appetite for borrowing, apart from blue-chip companies buying back shares, monetary policy doesn’t help.

The real problem with QE, though, is what happens when the Balance Sheet Recession finally ends. After years and years of Quantitative Easing, trillions of dollars’ worth of reserves have built up in the banking system, and also on central bank balance sheets.

All of those trillions are not a problem as long as the private sector is comatose. When nobody wants to borrow, trillions in excess reserves are like underground pools of water, or perhaps like wet gunpowder. They don’t circulate through the economy, and they don’t ignite inflation.

But at some point, when the private sector wakes up again and returns to aggregate borrowing, the situation changes dramatically. At that point, you get competitive demand for investor funds drawing down on trillions’ worth of reserves — which can lead to explosive inflation.

The net result of this, as Koo explains, is that getting out of the “QE trap” becomes an even bigger problem than beating the Balance Sheet Recession.

If the government implements enough fiscal spending to reignite the economy, as such that corporations want to start borrowing and spending for growth again, they simultaneously wind up activating the trillions of dollars in liquidity reserves that were previously stagnant, having built up via years and years of QE.

That, in turn, creates a threat of explosive inflation — which is also a threat via concerns of currency debasement — which then in turn forces the central bank to raise interest rates in order to head off inflation risks.

But of course, the central bank can’t raise inflation rates too quickly when the economic recovery is vulnerable — because if they try, the markets will crash and the economy will slip back into downturn or recession status.

In 2014 the Federal Reserve tried to “normalize” interest rates, the markets fell sharply, and they had to back off. In December 2018, the Federal Reserve under Jerome Powell tried again, with the same result: They tried to normalize monetary policy (take things back to normal), the markets freaked out, and they had to back off.

Okay, so how do we get out of the Balance Sheet Recession and the QE trap associated with it? The short answer is, we don’t really know and neither does anyone else — this is another one of those brand new things, nobody has ever tried to exit a ZIRP and QE regime — but we wouldn’t be surprised to see gold in the $10,000 per ounce range and Bitcoin well into six figures, many years from now, by the time all is said and done.