Many Americans are looking forward to traveling for the holidays to see family and friends, after lockdowns and COVID-19 waves hindered their plans last year. But the airline industry is facing a new problem. The current labor shortage could create another set of challenges for an industry in need of recovery.

Many Americans are looking forward to traveling for the holidays to see family and friends, after lockdowns and COVID-19 waves hindered their plans last year. But the airline industry is facing a new problem. The current labor shortage could create another set of challenges for an industry in need of recovery.

I spoke about a few of the changes COVID-19 is bringing, such as the shift to working and living remotely and the economic consequences. Today, let’s look deeper at another one of these trends: the future of delivery.

Today, many of us already think of the COVID-19 pandemic as another tragedy that “will live in infamy.” And while the pandemic and Pearl Harbor are very different in many ways, one thing is clear. Historians will look back at both as the beginning of considerable changes to our society and economy.

Today, I want to highlight a few advancements in Tesla’s battery storage business and explain why Tesla is quickly maturing into more than just a car company.

The central bank is poised to start the processing of tapering its balance sheet. However, the market doesn’t seem to be reacting negatively to the news. But I want to highlight yet another warning sign flashing red for the market. Let’s talk about the Fed, and then highlight this “alternative” signal for investors.

If this is a stock in your portfolio, you need to read the cold hard truth that I’m about to tell you. And if analysts are trying to convince you that now is the time to buy Alibaba… you also need to read this. It’s not time to touch this stock yet. Here’s why.

In 2016, a company you don’t associate with alcohol generated $1 billion in booze sales. Why am I pointing this out? Because this random fact drew my attention to a real buying opportunity.

As if the wholly unprecedented nature of political events and market extremes were not enough, we now must also contend with an era of weather extremes. For instance, have you ever heard of a wind-chill warning for North Texas? Probably not, because the U.S. National Weather Service has never issued one — until now. “The cold wind chills could cause…

Editor’s Note: TradeSmith offices are closed today to observe Presidents’ Day, but we didn’t want you to go without timely and interesting commentary. Our friends at LikeFolio have stepped up, and we will be back with regular TradeSmith Daily content tomorrow. For now, enjoy! —JCL When Shake Shack reports earnings on Feb. 25, it will be different than you’re used…

Inflation hawks need to relax, and perhaps even chill out a bit: The Magic 8-Ball forecast for when inflation roars back is still “Reply Hazy, Try Again.” That was the implied message of Jay Powell, the Chairman of the Federal Reserve, in a not-so-subtle pushback this week against rising fears that inflation will quickly become an economic problem. In no…

Tesla investors face many risks. One of the largest — and one of the least talked about — is China. Tesla has an extraordinary relationship with the Chinese government. Thanks to this relationship, Tesla enjoys privileges and perks no other American company has received. The question is how long the relationship will last. That question, in turn, is tied to…

The TradeSmith Decoder portfolio hit a new milestone this week. Our highest conviction equity position became a ten-bagger as of the Feb. 9 close, reaching the 1,000% gain mark in less than a year. The wild thing is, this company is just getting started. We wouldn’t be surprised to see it reach thirty- or forty-bagger status in the next few…

The Reddit rebellion appears to be over, or otherwise headed toward a quiet end. The GameStop squeeze is winding down — the share price of GME has stayed below $100 for days — and the Reddit silver squeeze appears to be winding down, too. In many ways, the GameStop saga was not what it seemed (for reasons we’ll examine shortly)….

Call it a strong hunch: There were people with advance knowledge of Tesla’s big announcement — and they used that knowledge to take large positions in Bitcoin, and Bitcoin-related equities, too. We don’t know these people, but we saw their footprints in the charts. A sizable tremor of buying activity rippled across all our Bitcoin-related holdings the Friday before last….

Did you dramatically increase your net worth in 2020, and book “life changing profits” while doing so? If not, you should consider TradeSmith Decoder, because at least one of our subscribers did (and possibly many more). We recently received a wonderful testimonial that illustrates what TradeSmith Decoder is all about: Helping people build real, life-changing wealth through the trading and…

Jeff Bezos, the founder-CEO of Amazon, announced this week that he was stepping down. This immediately caught our attention, as TradeSmith Decoder has held a stake in AMZN since April 2020. We’ve traded around the position multiple times, sometimes adding, sometimes booking partial profits. As of the Feb. 3 close, the core position is up more than 50%. For Bezos…

The stock market is both timeless and ever-changing, which makes it a curious paradox. On the one hand, markets look, feel, and behave exactly the same today as they did 100 years ago, or even two millennia ago. We can read stories of a bull market mania or market panic from the early 1900s, or the 17th and 18th centuries,…

The Great Texas Freeze Highlights a New Era of Weather Extremes

By: Justice Clark Litle

4 years ago | News

As if the wholly unprecedented nature of political events and market extremes were not enough, we now must also contend with an era of weather extremes.

For instance, have you ever heard of a wind-chill warning for North Texas? Probably not, because the U.S. National Weather Service has never issued one — until now.

“The cold wind chills could cause frostbite on exposed skin in as little as 30 minutes,” the National Weather Service advised shivering Texans. “Avoid outside activities if possible.”

The Dallas-Fort Worth area hit a low of 4 degrees on Monday. Meanwhile the day’s 14-degree high, registered around 4 p.m. at Dallas-Fort Worth International airport, was a full degree lower than the previous all-time low.

As Texans will tell you, that kind of thing isn’t supposed to happen. In parts of Texas, it is now colder than Alaska. That isn’t supposed to happen, either.

Texas has never experienced cold weather this extreme. Nearly 4 million Texas homes and businesses have experienced a loss of power due to rolling blackouts and utility outages, with approximately 650,000 additional homes and businesses facing outages in other states.

Then, too, Texas has not had rolling blackouts in at least a decade — since 2011 — and even then, power outage conditions are generally associated with the hot summer months, not the cold winter months, as air conditioning demand spikes in the midst of a heat wave.

Speaking of heat, 2020 was officially tied with 2016 as the hottest year ever recorded, dating back two full millennia and possibly far longer.

But rising global temperature levels don’t always translate to heat. Sometimes you get the opposite effect, as a result of abrupt shifts in atmospheric pressure and changes to longstanding air flow patterns.

For example, changes in the polar vortex — a large-scale area of low-pressure cold air around the Earth’s poles — have sent a wave of freezing Arctic air across multiple continents to kick off 2021. The global chill began weeks ago: Texans are only the latest group to feel frozen to the bone.

In Asia last month, spot rates for liquid natural gas (LNG) jumped 1,700% from the 2020 lows, triggering a spike in European gas prices to 12-year highs.

In the United Kingdom, the national grid was forced to issue emergency appeals for generator use, as wholesale electricity prices soared to nosebleed levels above $1,367 per megawatt hour.

In China, the lowest temperatures since 1966 are straining the electricity grid via spiking consumer demand for heat, even as LNG delivery and transport is disrupted by frigid weather.

In Japan, utilities are asking consumers to cut back on power consumption.

In Sweden, the largest single-day snowfall since 2012 left grids disabled and thousands of customers without power in January, forcing Sweden’s main utility to pay for hotel rooms as it struggled to restore power.

In Iran and Pakistan, natural gas shortages have triggered rolling blackouts as a result of heightened customer demand in the face of freezing cold.

The deep freeze in Texas is clearly part of a global pattern; the polar vortex is wreaking havoc.

The Texas freeze also matters to the rest of the United States, and the world, because of the direct impact on oil and gas production. Texas is the No. 1 oil and gas producer in the United States. More than 60% of East coast fuel supply comes from the gulf coast region, which is now being shut down by freezing weather.

An estimated 3 million barrels per day of oil-refining capacity has already been shut down, and oil-producing wells are being shut in to prevent water-freeze equipment damage in conditions of extreme cold.

The anticipated impact of the refinery and well shutdowns sent the price of West Texas Intermediate crude oil above $60 per barrel, to levels last seen in January 2020 (before the pandemic began).

Texas is having issues with renewable energy, too. Texas is a global leader in wind power, drawing 23% of its total power needs from wind last year — a larger amount than coal — but roughly half the state’s wind energy capacity has been shut down by freezing conditions.

Giant wind turbines can be outfitted with special equipment to stay operational in cold-weather extremes, but Texas never expected to need it.

The freewheeling nature of the Texas electricity system is also facing severe strain. Hundreds of thousands of Texans are facing crippling spikes in their electricity bills, due to open-ended arrangements where they pay for power at month-to-month spot rates.

Other Texans will find themselves completely without power when they need it most — as the inside of their home or apartment starts feeling like a refrigerator — with their original power provider either buckling under the weight of demand or charging astronomical spot-power rates, even as besieged competitors refuse to sign up new customers.

In terms of downstream consequences, the Texas freeze will add urgency to America’s need for a large-scale power grid overhaul and an overall green energy upgrade.

Texas itself will have to budget for expensive weather-proofing upgrades to its wind power systems, and Texas energy authorities will almost certainly have to deal with fierce consumer backlash after its deregulated electricity system fails a major test.

Then, too, America on the whole will have to prepare for an ongoing series of extreme weather events, and better take into account what that could mean nationwide — and what needs to be done to prepare.

The timing of the Texas freeze, and the hard lessons learned from it, will also play into the rollout of a multi-trillion-dollar infrastructure package allocated over several years.

A giant infrastructure initiative is likely to be the next big round of stimulus, to follow on the heels of the $1.9 trillion COVID relief bill now working its way through Congress; the Texas experience will underscore various line items needed to maintain energy security in this new era of extremes.

Can Shake Shack (SHAK) Deliver Huge Profits?

By: TradeSmith Research Team

4 years ago | Investing Strategies

Editor’s Note: TradeSmith offices are closed today to observe Presidents’ Day, but we didn’t want you to go without timely and interesting commentary. Our friends at LikeFolio have stepped up, and we will be back with regular TradeSmith Daily content tomorrow. For now, enjoy! —JCL

When Shake Shack reports earnings on Feb. 25, it will be different than you’re used to.

Normally, when a company reports earnings, everything about the prior quarter is revealed for the first time.

But in Shake Shack’s case, the company already let the cat out of the bag in its shareholder update on Jan. 12. SHAK reported 20Q4 revenues of $157.5 million – at the top end of analyst expectations.

This early reveal gave Wall Street a sigh of relief.

It proved that Shake Shack’s business was recovering in the wake of the pandemic.

As a result, shares of SHAK have soared to new all-time highs above $126.

Impressive. BUT….

Revenue is only part of the story.

There are still three very big questions lingering in the minds of investors that will be answered during earnings on the 25th… and could make or break Shake Shack’s big stock run.

Did Shake Shack Make A Profit?

While we already know the company’s revenues, it has not released how much spending was required to achieve those numbers.

At LikeFolio, we focus on consumer demand and generally don’t have insight into company spending levels.

With analyst expectations ranging from -0.16 to -0.06 per share, it seems unlikely that the company will have produced a profit in Q4.

But far more important than the company’s profit last quarter will be what the company says about the current quarter and the rest of 2021…

What is Shake Shack’s Outlook For 2021?

The market is unforgivingly forward looking.

That’s why you’ll sometimes see companies report blowout earnings, only to have the stock fall due to company revenue and profit projections that disappoint Wall Street.

In Shake Shack’s case, there is reason for concern.

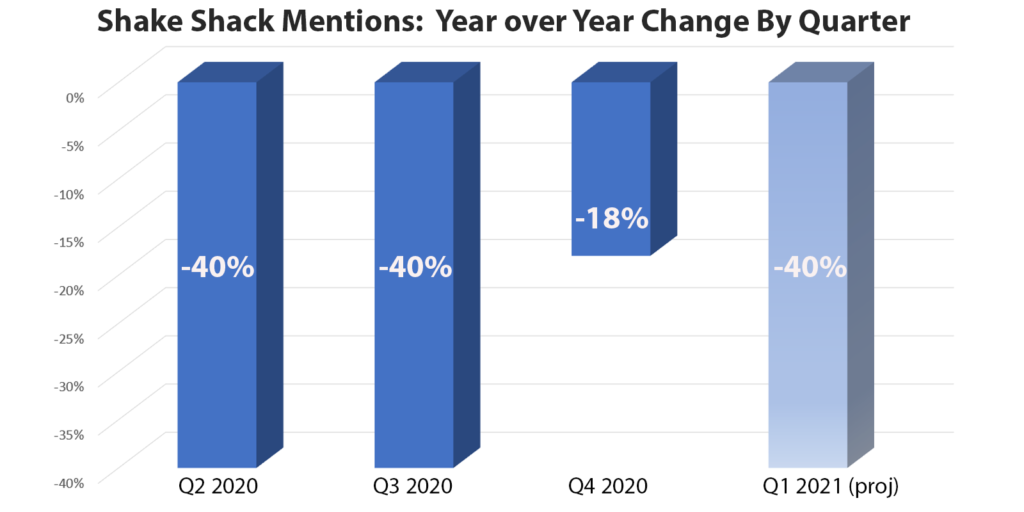

In the chart above, you can see that LikeFolio data accurately predicted the relatively strong Q4 revenue numbers that the company reported last month.

Wall Street saw that report as a signal that the company was starting to make a comeback following its massive revenue drops in the two prior quarters.

But when we look at the first six weeks of the current quarter, that “light at the end of the tunnel” starts to dim considerably.

This reversion back to a 40% decline in year-over-year consumer mention volume tells me that what happened in the last quarter of 2020 may have been an outlier and could actually be giving Wall Street a false sense of confidence regarding Shake Shack’s comeback.

So… what could have driven this “outlier” in Q4?

Has Shake Shack Become Dependent on Third-Party Delivery Services?

2020 completely changed the way consumers eat.

Instead of going out to restaurants, restaurants are coming home to us.

Third-party delivery apps have made meal delivery more popular than ever, giving consumers choices that they’ve never had before.

Instead of “which pizza place?” being the home-delivery question, it’s turned into “which restaurant?”

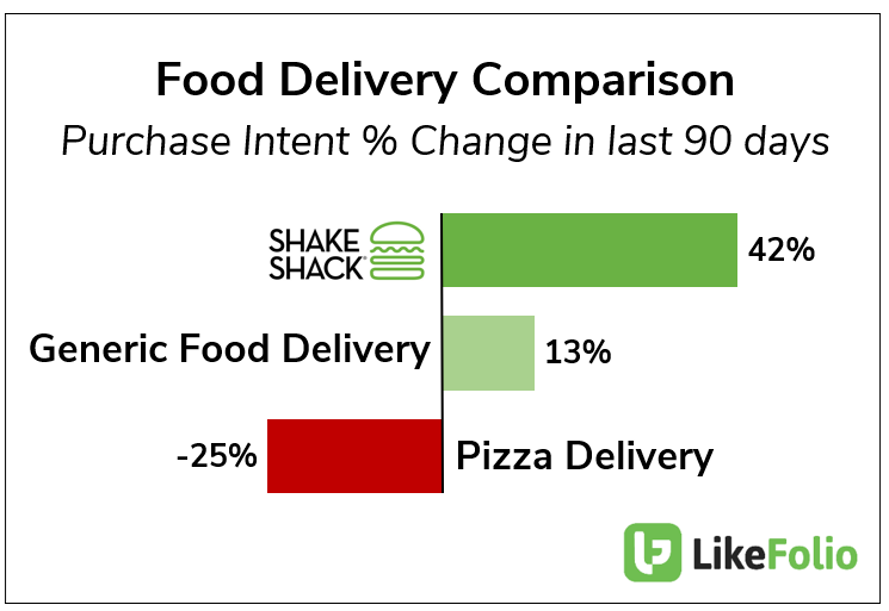

And companies like Shake Shack are benefitting in a big, big way:

Clearly, Shake Shack must be happy with a 42% increase in consumer demand for delivery of its tasty burgers and shakes. Any time you can outpace the overall trend (generic food delivery) by more than three-fold, you’re doing something right.

But third-party delivery is a double-edged sword.

On one hand, it makes Shake Shack’s product more accessible to a convenience-driven marketplace, increasing revenues.

On the other hand, third-party delivery introduces a middleman between Shake Shack and the customer, which not only reduces their control over the customer experience, but it costs money and can decrease profit margins.

This pressure on margins could become incredibly significant if it turns out that Shake Shack was pushing marketing dollars into third-party apps to improve its listing placements.

Playing Shake Shack (SHAK) From Here Summary:

SHAK stock is near all-time highs.

The good news about company revenues is already “baked in the cake.”

LikeFolio data suggests that consumer demand has already fallen back to the poor trends of Q2 and Q3 2020.

Shake Shack’s business in third-party delivery is booming but could weigh significantly on the profit margins that the company reports.

This all suggests Shake Shack investors could be in for a nasty surprise when the company reports earnings next week.

Fed Chairman Powell to Inflation Hawks: Chill Out For Now

By: Justice Clark Litle

4 years ago | Educational

Inflation hawks need to relax, and perhaps even chill out a bit: The Magic 8-Ball forecast for when inflation roars back is still “Reply Hazy, Try Again.”

That was the implied message of Jay Powell, the Chairman of the Federal Reserve, in a not-so-subtle pushback this week against rising fears that inflation will quickly become an economic problem.

In no small measure, that is our message, too.

As we have previously laid out in these pages, we certainly believe inflation — real, sustained inflation, of the type not seen for at least a generation — is coming at some point down the road. Signs of inflation’s return are already creeping in at the margins. You can almost sort of smell it, like the smell of rain before a thunderstorm.

But real and sustained inflation, of the type that truly disrupts economic activity, is probably months away; and could even be multiple quarters away; and might yet be a full year or two away.

Before getting to Powell’s remarks — and the nuance of expecting inflation later, but not sooner — we should touch on the topic of market timing.

In trading and investing, timing matters a great deal. That is because being too early, or too late, can have the same de facto impact as being wrong in terms of portfolio profit and loss.

Being too early on an investment theme, or an acted-upon market expectation, can mean getting discouraged and exiting with a loss before the actual move plays out; whereas being too late can mean only getting table scraps, or worse yet, missing the meal while receiving the bill.

What’s more, timing is often assumed to be a trader’s concern more-so than a patient investor’s concern. But that is not accurate, as patience only goes so far. The timing factor matters, even when it comes to longer-term trends and big picture investment themes — it just plays out on a larger scale.

To put it another way, timing matters for the long-term investor not with respect to incremental price changes, but the anticipated timing of a major shift in trend.

Consider, for example, the investor who behaves as if systemic inflation will show up in two months, when in reality it might not be due for 20 months.

That investor could allocate their portfolio heavily toward inflation-related investment plays — and then feel disappointed and dispirited when the value of his holdings goes down, rather than up, for months or quarters on end.

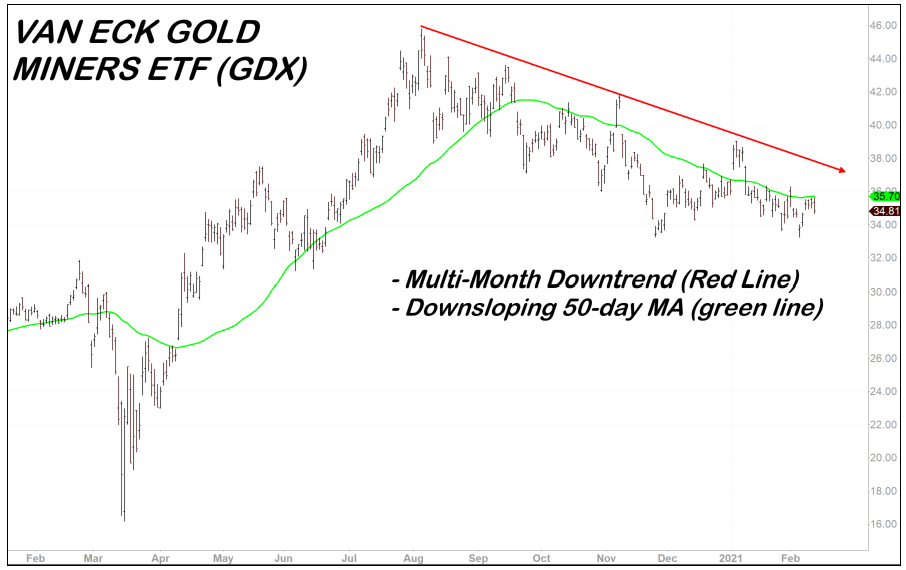

As an example of this, take gold stocks as represented by GDX, the bellwether gold stocks ETF. Gold stocks are in a downtrend right now and have stayed in one for months. We can see this with a glance at the GDX chart.

Gold stocks as a group (as represented by GDX) broadly peaked in August 2020, as did the gold price. Gold-related investments have been in a downtrend ever since, as defined by a series of lower highs and lower lows for GDX, coupled with a down-sloping 50-day moving average (the green line on the chart).

For the investor who is long-term bullish on gold stocks, the question is, when will the broad trend turn up again? Time will tell, and inflation (or a persistent lack thereof) will be a key factor.

Perhaps the back-to-bullish trend turn for GDX will come in three weeks; or perhaps it could be three months; or perhaps it could be 30 months.

That window of possibility as to when the trend could turn up again — from three weeks to 30 months, to roughly illustrate an order of magnitude — is far too wide for our taste.

Some investors will say: “We like gold stocks; we don’t mind waiting.”

We prefer to say: “You know what? We’ll check back in with gold stocks when the trend actually turns. Whether that happens in April 2021 — or, say, December 2022 — we’ll deploy capital elsewhere in the meantime.”

Timing! For way too many economic pundits and market commentators, timing doesn’t matter, because they aren’t putting real money to work.

But as the GDX chart demonstrates, for those who actually trade and invest in pursuit of profits, timing is a big deal, because a capital deployment effort misjudged by months, quarters, or even (gulp) years can be a very costly thing.

Getting back around to inflation — and soon enough to Powell — we anticipate inflation’s return, but not necessarily right away. It will probably take time for various inflation pressures to build up, and there will be moderating forces that push back against it.

Take the lingering impacts of the pandemic, for example.

The lower half of the U.S. economy, and the small business landscape overall, has been devastated by COVID. Trillions of dollars in new fiscal stimulus — complete with “helicopter drops” of direct payment — will help overcome that devastation, and likely produce inflation as a longer-term result.

But in the meantime, lingering economic pain could act as a moderating force that pushes back against inflation pressures, even as stimulated recovery efforts generate real economic growth.

Fiscal stimulus is an inflationary force aimed at overcoming COVID-related pain; but the OVID-related pain will itself absorb some of the inflationary pressure, allowing for growth without inflation early on (and the inflation bill coming due later).

Or consider the impact of rising yields at the long end of the U.S. Treasury curve:

A sustained rise in the 10-year and 30-year U.S. treasury yield is seen as ominous for the government debt burden, because the higher yields go, the higher the debt-service cost becomes (as expressed by interest payments on the national debt).

But rising yields at the long end of the curve, coupled with short-term rates near zero, are a very bullish development for banks, as the banks make money by borrowing at short-term rates and lending at long-term rates. The steeper the yield curve gets — a measure of short-term rates versus long-term rates — the more profits that accrue to the banking system, making banks more eager to lend.

Trillions in fiscal stimulus will add to the debt burden, but it will also spur real economic growth in at least two ways: Money that goes into the pockets of consumers and small businesses will be immediately spent; and banks will have increasing willingness to lend in the midst of a real recovery.

To put that more simply: If growth comes first, and inflation comes later, then the smart move is to invest in growth-oriented areas of the market, rather than inflation-oriented areas of the market.

Real economic growth is good for “reflation plays” related to areas of the market like industrials and consumer goods; it is not so great for inflation havens like precious metals. Inflation is just the opposite — it is good for inflation havens like precious metals, but not so good for growth-oriented reflation plays.

Getting that mix right — anticipating the mix of real economic growth versus inflation, when coming out of a recession and a pandemic, with a cartoonishly expanded money supply and trillions of dollars in fiscal stimulus at work — is a very tricky thing.

It is such a tricky thing, in fact, that we would rather defer to the market’s opinion (as expressed through charts and price action) than be overly confident in our own assumptions.

On that score, were inflation a truly imminent concern, the gold price would be trending higher (it has been trending lower for months); the 10-year U.S. Treasury note would have a yield above 2% (instead it is modestly above 1%); and inflation-vulnerable areas of the stock market, like utilities, would be experiencing price dislocations and downtrends (they are not).

So why are inflation hawks getting flustered too early? In our view — or rather, our interpretation of the market’s view — they are missing the concept of “growth first, inflation later” and putting the cart before the horse.

The horse is named “growth and recovery,” the cart is named “inflationary consequences”, and the horse is supposed to come first, dragging the cart along behind it, with the contents of the cart to be unloaded at a future time.

Areas of the market that could forecast either real economic growth or signs of inflation, depending on one’s interpretation — we speak here of the oil price and copper price, to give two examples — thus deserve the growth interpretation, in our view, rather than the inflation interpretation, because adjacent areas of the market that express pure inflation concerns (e.g. precious metals) are not at all doing well.

As such, we interpret price signals like Brent crude above $60 per barrel, and the copper price trading at nine-year highs, as the market’s anticipation of real economic growth — because that is what the market itself is saying, by way of the current price mix.

And that mix is wholly commensurate with, drumroll please, a stimulus-driven economic recovery that presents growth now, and a nasty inflation bill later — with the timing on “later” being measurable in months, or quarters, or possibly even a year or two.

Timing again! This isn’t just a fun puzzle for those who enjoy the intellectual aspects of putting the pieces together; it is also a puzzle that can make an investor rich, if they can determine the proper sequence of actions (deploying capital not just to the right mix of places, but also at the right time).

Our willingness to defer to market judgment as expressed through price signals makes it easy to agree with Jay Powell, Chairman of the Federal Reserve, in his not-so-subtle suggestion this week that newly minted inflationists are jumping the gun.

Chairman Powell’s “stop fretting over inflation” message was delivered on Feb. 10 in a speech to the Economic Club of New York.

Here is the part where inflation concerns were dismissed:

“You could see strong spending growth, and there could be some overt pressure on prices. My expectation would be that will be neither large nor sustained. Inflation dynamics will evolve but it’s hard to make the case why they would evolve very suddenly in this current situation.”

Translation: An economic recovery will drive spending growth, which in turn could push prices up — but that isn’t the same as sustained inflation, which will take a while to get going, so don’t sweat inflation for now.

In the same speech, Powell emphasized the importance of helping out the labor economy, which means taking aggressive action to get struggling Americans and small businesses back on their feet:

“A strong labor market that is sustained for an extended period can deliver substantial economic and social benefits, including higher employment and income levels, improved and expanded job opportunities, narrower economic disparities, and healing of the entrenched damage inflicted by past recessions on individuals’ economic and personal well-being.

At present, we are a long way from such a labor market. Fully realizing the benefits of a strong labor market will take continued support from both near-term policy and longer-run investments…”

Translation: We’ll all be better off when recovery benefits are widespread, and a stronger labor market will mean a stronger economy on the whole.

The second part, about helping the labor market, is also a “don’t worry about inflation” message because, to the extent policy drives real economic growth, income and yields and prices can rise without inflation becoming a problem.

To be sure, we think the Federal Reserve and Treasury will lose control of the inflation narrative at some point.

The U.S. government’s willingness to help the economy through brute force, via the unleashing trillions of dollars in monetary and fiscal support, will eventually touch off the kind of inflation pressures America hasn’t seen since the 1970s, or even the late 1940s in the aftermath of World War II.

But the key word there is “eventually.” In the near to medium term, market price signals seem to back Powell’s stance: Growth and recovery is the part that comes next, with inflationary consequences postponed.

Will the Chinese Government Kneecap Tesla?

By: Justice Clark Litle

4 years ago | News

Tesla investors face many risks. One of the largest — and one of the least talked about — is China.

Tesla has an extraordinary relationship with the Chinese government. Thanks to this relationship, Tesla enjoys privileges and perks no other American company has received.

The question is how long the relationship will last. That question, in turn, is tied to national strategic interest as defined by the Chinese government.

If the Chinese government decides it has gotten what it wants from Tesla — or that strategic interest favors playing hardball, rather than continuing to offer favors — things could go bad very quickly.

And to get a sense of how ugly a soured relationship with the Chinese government can be, just ask Jack Ma, the founder of Alibaba and Ant Financial group — or the institutional investors who stand to lose billions as a result of the scuttled Ant Financial IPO.

It would not surprise us if something comparably nasty happened to Tesla.

The topic is timely because, shortly before Tesla’s big Bitcoin reveal, a slightly alarming piece of news came out of China. “Tesla Summoned by China Regulators Over Quality, Safety Issues,” Bloomberg reported on Feb. 8.

“Authorities including the State Administration for Market Regulation held talks with Tesla’s Beijing and Shanghai units,” said Bloomberg, “after customers complained of problems including abnormal acceleration and battery fires… Tesla was asked to improve internal management, comply with Chinese law and regulations and protect consumers’ rights.”

Ah yes, the old tap on the shoulder from regulators. That is the treatment Jack Ma got, right before his $34 billion IPO was killed.

China’s electric vehicle (EV) market is large and sprawling, and it had more than 500 competitors at one time.

The strategic consensus is that the Chinese government welcomed Tesla into this fray to, first, serve as a best-practices example for homegrown EV makers to learn from and copy; and, second, to help ramp up local supply chains and make China’s EV ecosystem more robust.

Once those two purposes are served, the Chinese government may find it has no more use for an American automaker dominating the local EV sector.

Once China’s EV ecosystem is robust, and national champions like Xpeng and NIO have become strong, the Chinese government may decide to kick Tesla to the curb, or pose a “take it or leave it” ultimatum that involves nationalizing Tesla’s technology and intellectual property, or force Tesla into driving down prices until profit margins hit zero (as an alternative to taking huge losses).

In simple terms, what Tesla investors do not realize is that the Chinese government is a cat, and Tesla is a mouse. For the moment, the cat is content to let the mouse have its cheese.

When that state of affairs changes, it won’t be good for the mouse.

What’s more, the tap on Tesla’s shoulder from China’s state regulators — who hold so much power they might as well be mafia bosses — suggests the cat is preparing to pounce.

A major setback in China, created by the Chinese government, would pose a severe threat to Tesla on multiple fronts.

First, it could mean the potential loss of one of Tesla’s largest EV markets (if not the largest, bar none); second, it could mean the elevation of a homegrown EV champion (like Xpeng or NIO) at Tesla’s expense, not just in China but globally; and third, it could mean a transfer of intellectual property and technology to some of Tesla’s fiercest EV competitors.

To fill in some backstory, Elon Musk is beloved as a kind of entrepreneurial folk hero by the Chinese people, and the Tesla Model 3 was the most popular electric vehicle in China for much of 2020. Tesla China sold 120,000 vehicles last year; the Model Y is heading into Shanghai production alongside the Model 3; and China-based Tesla production is expected to ramp up considerably.

All of this matters — a lot — because China is the biggest EV market in the world by a large margin, thanks to an aggressive, decade-plus push by the Chinese government to promote electric vehicles over internal combustion engine (ICE) vehicles.

In Shanghai, for example, the license plate registration fee for an ICE vehicle is $14,000, but EV license plates are free. The Chinese government also exempts most EVs from a 10% tax on new vehicles, and further offers hefty purchase subsidies to make EVs affordable to Chinese consumers.

In 2015, Tesla was importing American-made vehicles into China, and it wasn’t going all that well. They were only shipping a few thousand cars per year, and large gaps existed in Tesla’s knowledge of the local Chinese market.

But then, in the years that followed, Tesla saw the opportunity to make a sweetheart deal with the Chinese government.

As a result of the Trump administration’s tough-on-China stance, and the perception of unfair treatment for American companies doing business there, China was losing its appeal as a destination for investment.

Just as the Chinese government truly started worrying about the U.S.-China trade relationship, Tesla came knocking with its proposal to build vehicles in China.

Strategically, the Tesla deal offered big advantages to China on two fronts: It could serve as a high-profile example of an American company enjoying success and good treatment in China — which would help the U.S.-China trade relationship — and Tesla’s presence could help invigorate the local EV ecosystem, as previously explained.

In service to its own strategic interest, the Chinese government thus went to extraordinary lengths to make Tesla happy. In every prior case, foreign automakers had to do a joint venture with a local Chinese counterpart and couldn’t own more than 50% of any China operation; Tesla was exempted from that rule.

Then, too, Tesla’s Shanghai plant was approved and built in record time, relative to the normal timeframe for companies to get regulatory approval, local and regional licenses, power and electricity hook-ups, and so on. As if that weren’t enough, Tesla also received billions in low-cost financing from state-owned Chinese banks, and Tesla vehicle purchases were made eligible for government EV subsidies.

All in all, Tesla had received just about every favor and fast-track initiative one could think of by the time the Tesla Shanghai plant broke ground in 2019. There was also a two-way flow of mutual respect and admiration: Elon Musk declared that “China rocks” in a podcast interview, and a local official offered Musk permanent China residence.

All of this sounds great, until investors remember what happened to Jack Ma — another entrepreneurial folk hero who seemed to have the blessing of the state.

Everything turned up roses for Ant Financial and Alibaba, until the day it suddenly didn’t.

The reason we anticipate a comparable turning of the tables for Tesla — besides the aforementioned tap on the shoulder from regulators — is because the reason for Tesla’s super-favorable treatment is clear, and the natural incentive to reverse that treatment is also clear.

When the cat decides it is more strategically advantageous to kill the mouse, or terrorize it with harsh demands, the picture for Tesla’s China operations could change instantly. Again, we’ve already seen a shocking version of this; Jack Ma could tell you about it, were he still talking.

Gold Now Looks Bearish — and the Dollar Bullish — because of the Quantum Deficit Effect

By: Justice Clark Litle

4 years ago | Investing Strategies

The TradeSmith Decoder portfolio hit a new milestone this week. Our highest conviction equity position became a ten-bagger as of the Feb. 9 close, reaching the 1,000% gain mark in less than a year.

The wild thing is, this company is just getting started. We wouldn’t be surprised to see it reach thirty- or forty-bagger status in the next few years.

Nor is it just the one position. There are other names in the portfolio — all long-term holdings of meaningful weight — up more than 205%, 584%, and 750% as of the Feb. 9 close.

There are also two more equity holdings up more than 100%, and four additional ones up between 35 and 60%, spanning an industry range of crypto, copper, solar, oil and gas, and more.

To see gains like these across the board — with a real potential for more — a powerful bull market is required. And right now, investors are experiencing one of the biggest bull markets of all time.

This brings us to gold, which looks terrible, and the U.S. dollar, which looks strong.

A great many financial editors are bullish on precious metals these days. We are not. In fact, we would not be surprised to see the gold price drop 25% or more over the course of the next year.

If you are the type of investor who prefers to keep a gold allocation no matter what, that is all well and good. Gold will rise and shine again, in our view. But if you are going to hold, be psychologically prepared for a significant amount of pain over the next few quarters.

The wide-ranging equity bull market, and the deteriorating outlook for gold, are related to each other, for reasons we shall soon explain.

We also see a significant possibility the U.S. dollar could strengthen, by a meaningful amount, over the next few quarters. This could surprise a lot of people — especially those expecting the precious metals complex to rise rather than fall.

It’s a very strange environment. And the picture could change quickly. But we are going by what we see and understand, and updating our views as events unfold in real time.

To clarify something important, we are long-term bullish on gold and long-term bearish on the U.S. dollar.

Over the next few years, we fully expect the price of gold to rise by a lot — and the value of the U.S. dollar to fall by quite a lot.

But in the medium-term, and possibly for the next few quarters, we are more inclined to see the opposite — a strengthening U.S. dollar, and a weaker gold price — because of the Quantum Deficit Effect.

The “Quantum Deficit Effect” is our name for a theory developed by George Soros, the founder of the Quantum Fund, and Stanley Druckenmiller, a long-time portfolio manager of the Quantum Fund and one of the greatest money managers of all time.

The Quantum Fund was a pioneer in the “global macro” style of hedge fund investing, reportedly earning 33% annual returns over a period of 30-plus years.

Stan Druckenmiller, who managed money separately while also running the Quantum Fund for Soros, is also known for earning better than 30% years over decades — with no negative calendar years, ever, since 1981.

Think how good a money manager has to be to never lose money, on a calendar basis, for 40 years straight, while routinely shooting the lights out. That is what Druckenmiller was (and still is) known for.

The Quantum Deficit Effect — which is not an official name, but our own descriptive reference — is a theory that was first put forth by Soros in the 1980s, in his book The Alchemy of Finance.

It is no ordinary academic-style theory, however. Academic theories don’t generate billions of dollars in profits on currency trades, and this one actually did. Soros and Druckenmiller used the theory, on more than one occasion, to score billion-plus wins in gigantic forex trades.

It applies today because, if 2021 plays out the way we think it could, the Quantum Deficit Effect could be responsible for a surprise strengthening in the dollar, even as the U.S. budget deficit expands.

The theory had its origins in the big budget deficits of the Reagan administration.

Because the Reagan administration was spending heavily to win the Cold War, and budget deficits were rising, there was a widespread belief that the U.S. dollar would weaken, or even fall precipitously.

But Soros saw things differently. He thought that, if deficit spending is coupled with tight monetary policy and economic growth, the currency would be more likely to strengthen than to weaken.

If monetary policy is tight — or heading in a tighter direction — and deficit spending is contributing to economic growth, then capital is likely to flow into a recovering economy, and into its bonds, as interest rates rise at the long end of the curve.

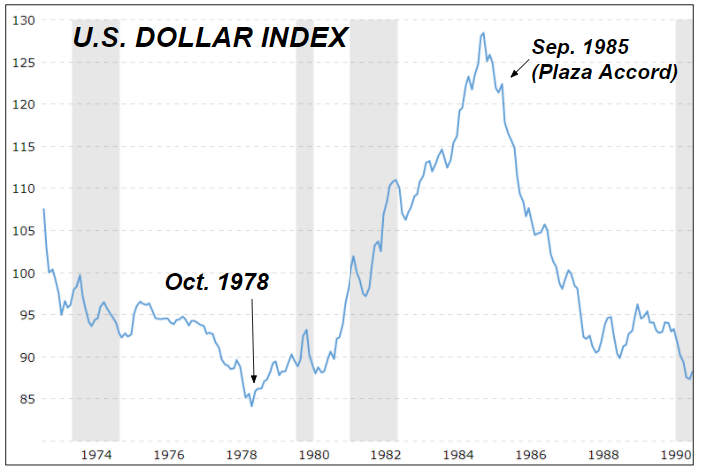

The theory helps explain why the U.S. dollar bottomed out in October 1978, and then rose relentlessly in value until March 1985, at which point the dollar’s relentless strength had become a real problem.

In September 1985, a coordinated central bank policy intervention, known as the Plaza Accord, was agreed to by the G5 — the United States, Japan, Germany, the U.K., and France — to push the value of the dollar lower.

You can see the dollar’s seven-year rise, powered by a cocktail of tight monetary policy, budget deficits, and economic growth, in the chart below via macrotrends.net.

As the manager of Quantum Fund, Druckenmiller used this theory to book a gigantic forex win in the German deutsche mark after German reunification in 1990.

When the Berlin Wall fell in 1989, and West Germany prepared to reunite with East Germany, the popular consensus was that the deutsche mark, Germany’s currency, would weaken, because German budget deficits were about to explode as a function of reunification.

The thought was that West Germany, a rich country, would have to spend a lot of money to help East Germany, a poor country, catch up to Western norms. That meant budget deficits, which meant the deutsche mark should weaken.

But Druckenmiller, like Soros, understood that tight monetary policy coupled with budget deficits could be bullish for the currency, not bearish — and he knew that the German Bundesbank was likely to tighten up substantially to avoid inflation. So, Quantum Fund bought the deutsche mark as a bullish forex trade, even as others were selling it, and made a lot of money on the position.

So, the gist of the Quantum Deficit Effect is as follows:

Big budget deficits do not automatically mean a weaker currency. If budget deficits are coupled with tighter monetary policy and economic growth, the currency can actually strengthen.

A combination of economic growth, higher interest rates (through tighter policy), and a more hawkish monetary stance can all combine to push the value of a currency higher, rather than lower, even as budget deficits are expanding.

And now, with those details explained, we can cycle back around to the current backdrop, which now looks bullish for the U.S. dollar and bearish for gold — at least temporarily anyway.

Investors are anticipating a vaccine-powered global recovery. There is no question this is happening. A few elements that demonstrate this are as follows:

U.S. equity markets, and various indexes around the world, are at all-time highs.

The U.S. yield curve, a barometer of economic bullishness, is at its steepest point since 2015, indicating greater expectations of economic growth than any point seen in the past six years.

The yield on the U.S. Treasury 30-year bond surpassed 2% for the first time since the pandemic began, again indicating more belief in a long-term inflation and growth pick-up.

The price of Brent crude oil, a barometer of global economic activity, has surpassed $60 per barrel, and traded above its 200-week moving average, for the first time since the pandemic began.

Junk bond yields touched their lowest levels ever — falling below 4% — indicating speculative appetite for growth-oriented credit even as long bond prices fall and long-term interest rates rise.

The debate over the coming $1.9 trillion stimulus package — likely to be pushed through via budget reconciliation — has centered around inflation, and fears of inflation.

With all of the above happening, COVID-19 cases are also declining in the United States.

“Newly reported cases have dropped 56% over the past month,” the Wall Street Journal reports, adding that hospitalizations have fallen 38%.

Meanwhile the seven-day average for positive COVID tests is at its lowest since Oct. 31, and vaccine rollout efforts are ramping up. The Defense Production Act has been utilized, and the U.S. might even see military medics administering shots in NFL football stadiums.

Then, too, they are sending everyone money. The next round of $1.9 trillion stimulus will include another “helicopter drop” of cash sent to households — the biggest one yet — coming on the heels of prior helicopter drops that helped boost personal savings rates to multi-decade highs during the pandemic.

All of this means the following is highly likely over the next few quarters:

We are going to see accelerated growth coming out of the pandemic, turbo-boosted by the combination of vaccine rollouts and a new $1.9 trillion stimulus.

This growth will come at a time when American consumers are flush with cash and ready to spend it, especially after being cooped up in a pandemic, and furthermore at a time when commercial bank deposits have exploded.

U.S. banks will be ready to lend in this environment — and there will be plenty of attractive growth opportunities, as corporate franchises that survived the pandemic with strong balance sheets intact see an opportunity to expand into areas that dying small businesses left behind.

U.S. treasuries will sell off at the long end of the curve — with a real possibility the 10-year yield could double, from 1%-plus to 2%-plus. The 30-year could also rise significantly, or even double to 3 or 4%.

“Inflation” will become a new buzzword — this is already happening at lightning speed — and the Federal Reserve will adopt a tighter monetary stance, not by raising rates, but simply by pulling back on their bond market support efforts.

“How can the Fed tighten?” you might ask. “Isn’t the recovery too weak for monetary policy to get tight?”

The answer is that the Federal Reserve is likely to keep short-end rates at zero. They certainly won’t engage in any interest rate hikes and have promised not to do so for years.

And yet, the Federal Reserve can tighten up monetary policy simply by doing less of what they were doing all throughout 2020.

If the Fed was a big buyer of U.S. Treasuries in 2020 — which they were — and they buy far fewer Treasuries in 2021, that is a form of tightening. Easing off the accelerator is directionally a hawkish thing to do, even without stomping on the brake.

All of this is bullish for the dollar, bullish for U.S. equities, and very bad for gold.

Then, too, Europe is falling behind in the COVID recovery race.

For a whole host of reasons, some of them surprising, Europe has bungled the vaccine rollout, which means their recovery pace is likely to stumble, or even fall into a new recession, even as the U.S. pulls out of recession by way of vaccine rollout progress, renewed commercial lending, and a gargantuan boost of fiscal stimulus.

And then, last but not least, inflation fears will prove premature.

Serious inflation will come — we are very much expecting that — but it will take a while to get here.

Those who anticipate inflation right away are mistaking a clear view for a short distance, in the words of futurist Paul Saffo.

In the near-term, a large amount of fiscal stimulus will be absorbed by consumers paying down debt, or catching up on rent, and it will also take time for capital expenditure spending to ramp up again.

That means, in the near-term, we could see mostly inflation-free growth, or growth with very mild inflation, coupled with rising yields at the long end of the curve.

In a world where Europe is slumping due to COVID missteps as the United States moves back into growth mode, that is, once again, very bullish for the dollar — and very bearish for gold.

This is also a recipe for a continuing equity bull market. What happens when a flood of new currency comes into the system (via stimulus), but inflation is delayed (because it takes a while to show up), and investors remain excited about growth opportunities as capex picks up and banks start to lend?

You get valuations that push higher, simply because there is more currency available, in the pockets of savers and investors, that winds up going into the market. And you also have private equity firms, sitting on giant piles of cash remaining to be deployed, that still need to find their way into investment opportunities, and special-purpose acquisition company (SPAC) capital raises adding billions of dollars per week.

Eventually the script flips back again — against the dollar and in favor of gold — because the U.S. economy will have to pay for this fiscal tsunami of stimulus.

The tricky part is that the inflation bill is not immediate — rather it comes due further down the road. You get the growth boost first and the headache later, sort of like financing business expansion with credit card debt. Happiness leads and the sting is in the tail.

To state it plainly: Big fiscal stimulus now, in the presence of an organic, vaccine-powered recovery, can mean healthier growth now, but much worse inflation farther down the road.

That is why, longer term, we are raging dollar bears and committed precious metals bulls.

But in the near term the vaccine-powered recovery, coupled with the Quantum Deficit Effect, looks likely to generate growth in the United States, coupled with tighter monetary policy, rising long-end rates, and global capital flows attracted to U.S. credit, U.S. equities, and U.S. expansion opportunities.

Aftermath Lessons from the Reddit Rebellion

By: Justice Clark Litle

4 years ago | Educational

The Reddit rebellion appears to be over, or otherwise headed toward a quiet end.

The GameStop squeeze is winding down — the share price of GME has stayed below $100 for days — and the Reddit silver squeeze appears to be winding down, too.

In many ways, the GameStop saga was not what it seemed (for reasons we’ll examine shortly). But it was, certainly, one of the wildest market events of the past 100 years.

To find a comparable drama, one has to revisit the Volkswagen short squeeze of 2008 — an event that cost hedge funds tens of billions in aggregate. Going back further, one can look at the Hunt brothers’ attempt to corner the physical silver market in 1979-80.

And yet, both of those events were different in their own way. One was executed by a corporate insider (Porsche), and the other attempted to hoard a physical commodity (silver) without full control of the futures markets.

To find a comparable short squeeze that could be called retail versus the establishment, or man against Wall Street, one has to revisit the early 1920s and the battle of the Piggly Wiggly.

The Piggly Wiggly supermarket chain was founded as the first “self-serving store” in 1916, and there were more than 600 outlets by 1921. Piggly Wiggly stores are still in operation today, with more than 530 locations across 17 states.

Nearly 100 years ago, in 1923, the outlook for Piggly Wiggly had turned bearish, and Wall Street was ganging up on the stock. The repeated bear raids greatly irritated Clarence Saunders, Piggly Wiggly’s founder and CEO — and Saunders decided to fight back.

Saunders went after the bears by engineering a massive short squeeze of Piggly Wiggly stock. Saunders loaded up on debt to finance the purchase of all the Piggly Wiggly shares in the open market, leaving the shorts high and dry.

But the exchange changed the rules on Saunders, much as brokers like Robinhood changed the rules on buyers of GameStop. Instead of requiring the shorts to close their positions within a certain timeframe, the obligation to cover was suspended.

The delay in getting the shorts to cover then worked against Saunders, who lacked the capital for debt service payments after leveraging up to buy all the Piggly Wiggly shares. Eventually Saunders cracked (for lack of ability to carry the debt), and the Piggly Wiggly corner was broken.

It’s hard to bet against the establishment, mainly because the establishment can change the rules. The Hunt brothers found this out the hard way, too, when the Chicago Mercantile Exchange (CME) made it impossible to keep the squeeze going in silver futures.

In a similar way, we won’t know what might have happened if the brokerage firms not restricted GME buying in a critical time window. They did it to save their own skins for lack of equity capital, but still — you have to wonder.

Either way, there are numerous potential lessons to draw from the GameStop drama. Let’s look at a few of them now.

The Popular Narrative is All Too Often Wrong

When Robinhood first restricted trading in GME, the immediate assumption was that they were doing the direct bidding of firms like Citadel, or otherwise trying to help the hedge funds that were short.

Dave Portnoy, a prominent sports-bettor-turned-day-trader with a large online following, even said he thought Robinhood’s actions were criminal and that the CEO should go to jail.

In reality, Robinhood more or less panicked because of a firm-wide margin call. Robinhood didn’t have the necessary clearing capital on hand to handle the incredible volume of GME call options and shares being purchased, with financial risks being amplified by the two-day settlement process known as “T+2.”

But Robinhood couldn’t admit to its margin call state of affairs outright — at least not at first — for fear that the billions in new capital they need to raise would not be available if investors were scared off. (The best time to raise capital is when you don’t really need it; if a financial entity is seen as desperately needing capital, there is a fair chance it dies.)

Big problems certainly existed in the way Robinhood handled things, and upcoming congressional hearings will likely shed some light on that. But the narrative that dominated the headlines, and the hot takes of the politicians on both sides of the aisle, was wrong.

Hindsight is Not 20/20

There is an old saying that “hindsight is 20/20,” implying that everything is clear in the rear-view mirror. But this often isn’t true: It can be just as hard to analyze the past as it is to guess the future..

In a complex system with a swirling mix of variables, and especially when many of those variables were never before seen — like zero-commission trading, trillions of dollars in stimulus, the gamification of online trading apps, and so on — it can be very hard to see what is coming.

The thing is, it is also hard to see what just happened. Not only can complexity create an impenetrable fog of war in terms of upcoming future events, it can do the same with events that already happened.

Take the assumption, for example, that the hedge fund shorts won and the Redditors lost. This is somewhat accurate in certain respects, but in other respects it isn’t true at all.

We can first note that some in the Reddit army did spectacularly well.

For example Anubhav Guha, a 24-year-old graduate student at MIT, managed to turn a $500 stake into $203,411 in less than three weeks, according to the Wall Street Journal.

Guha’s early experiments with trading, near the start of the pandemic, were mostly failures, costing him half of an initial trading stake in the low thousands; but he more than made up for it with GameStop.

There were no doubt many others Redditors, though not necessarily a majority, who either scaled out or cashed out to sufficient degree to come out ahead on GME — in some cases way, way ahead.

At the same time, and in further contrast to the assumed narrative — long retail bulls versus short hedge fund bears— one of the biggest GameStop wins was a hedge fund wager on the long side.

Senvest Capital, a hedge fund formed in 1997, had started developing a bullish thesis on GameStop a full year earlier, based on fundamental analysis that suggested the bear case was overdone. By October 2020, Senvest had accumulated a substantial position amounting to nearly 5% of GameStop shares, at an average purchase price below $10 per share.

Senvest Capital then watched in awe as the GameStop squeeze unfolded, and when Elon Musk tweeted a single word — “GameStonk!!!” — the move got so heated they decided to cash out and book $700 million in profits.

So, a portion of Redditors won rather than lost; and some hedge funds won big from the long side, rather than the short side; and then, too, at least a handful of bearish hedge fund firms were decimated. Melvin Capital, a $12.5 billion fund, was down 53% in January due to losses on GME and other shorts, for example — and other large hedge funds also saw losses well into double-digit percentage territory.

That makes for a far more subtle hindsight wrap-up than just, “the hedge fund bears won and Reddit lost.”

It gets more subtle still when considering the fact that, even among the Redditors who walked away empty-handed, some of tomorrow’s great traders and investors could be among them. Failure can be a better teacher and motivator than success — especially for someone in their 20s and 30s.

If You’re Going to Bet the Farm, Have Two Farms

Some cautionary types say “never bet the farm.”

We prefer the expression: If you’re going to bet the farm, have two farms.

The translation is, sometimes it really does make sense to bet big; and yet, it rarely if ever makes sense to bet so big one’s financial and psychological well-being are at stake.

Those who never take bold risks run the risk of leading “quiet lives of desperation,” as Thoreau put it, having never truly tried for something.

Those who take risks they can’t actually afford, on the other hand, can put their own future, and the well-being of their family, in danger.

The better path, in our view, is to learn the art of the selective big bet, while coupling the rare “bet the farm” move with the science of smart risk management.

Some risks are worth taking, but only to the extent they can be safely done. One way to handle this is to think clearly about what’s at stake and to always have capital in reserve.

Don’t Go All or Nothing When You Can Take Some Off the Table

Another lesson from the GameStop spectacle is the value in avoiding “all or nothing” type situations, except when they are necessary.

By that meaning, a trader who was long GME, and had substantial gains at some point, could likely have cashed out a portion of their position large enough to take back their initial capital and show a profit; the capital still in play could then have participated in further upside.

There are certain types of financial wager — like buying a house, or selling a private company — where “all or nothing” is mandatory, in the sense that taking partial profits or splitting the difference isn’t really an option.

But when trading liquid assets like stocks, futures, forex, or cryptocurrencies, it is almost always possible, at some point in a significant winning trade, to reduce risk while still maintaining a useful exposure profile.

Being willing to scale in or out — not buying all at once, and not selling all at once either — will mean forgoing the glory of picking the exact moment when it was ideal to buy or sell. But the reward for trading discipline overall can be a more emotionally fulfilling experience, with fewer painful instances of “I wish I had sold” or, sometimes even more painfully, “I wish I’d stayed in.”

Someone Acted Early on Tesla’s Bitcoin Plan (We Spotted Their Footprints)

By: Justice Clark Litle

4 years ago | News

Call it a strong hunch: There were people with advance knowledge of Tesla’s big announcement — and they used that knowledge to take large positions in Bitcoin, and Bitcoin-related equities, too.

We don’t know these people, but we saw their footprints in the charts.

A sizable tremor of buying activity rippled across all our Bitcoin-related holdings the Friday before last. For TradeSmith Decoder subscribers, that led us to issue an “urgent Bitcoin buy alert” on Jan. 29.

Before getting into the buy signal details, we should clarify the news.

The Bitcoin price exploded to new all-time highs above $44,000 today (Monday, Feb. 8) on news that Tesla has purchased $1.5 billion worth of Bitcoin and intends to accept Bitcoin as payment.

Tesla revealed the Bitcoin news in a filing with the Securities and Exchange Commission (SEC), stating the BTC purchase would enable “more flexibility to further diversify and maximize returns on our cash.” Tesla also said it would accept Bitcoin for product payments “initially on a limited basis.”

As of year-end 2020, Tesla had more than $19 billion in cash or cash equivalents, which suggests the $1.5 billion Bitcoin purchase is worth roughly 8% of liquid assets.

It will be interesting to see how the SEC handles this situation — if they even take action at all, that is.

In recent days, Elon Musk has been promoting cryptocurrency more aggressively than ever before.

About two weeks ago, Musk changed his Twitter bio to say “#bitcoin,” as did a handful of other Silicon Valley heavyweights.

Shortly after that, Musk said the following in a social media chat: “I do at this point think bitcoin is a good thing, and I am a supporter of bitcoin.”

Talking up the value of Bitcoin — prior to one’s company announcing a Bitcoin initiative of blockbuster size and importance — could present an interesting dilemma for the SEC.

By the SEC’s own definition, Bitcoin is not a security, but rather more of a digital commodity. And insider trading isn’t a punishable offense with commodities.

The early buying of crypto-related equities, however, could be another matter, because insider trading laws very much apply to publicly traded entities.

And somebody was buying crypto stocks. We know this, because we saw their footprints — a groundswell of buying activity that showed up in the price action — and acted on it.

Below is a lightly condensed excerpt from the TradeSmith Decoder broadcast on Jan. 29, just a week prior to the Tesla bombshell:

An Urgent Bitcoin Buy Alert (For Those Still on the Sidelines)

Today was supposed to be a model portfolio update. We are pushing that back to Monday or Tuesday, however, to share a very important announcement:

It is now a good time to buy Bitcoin, and a good time to buy the Bitcoin-related names in our portfolio.

Recent developments — very recent, like all in the past 24 hours — have changed the Bitcoin picture dramatically, and created a window of opportunity to act for those still on the sidelines.

We don’t have official recommendations today because the Decoder Model Portfolio already has enough exposure…

With the above said, for those who are following along and don’t have enough crypto exposure — because you didn’t buy when we did, or you subscribed to Decoder in recent weeks, or for whatever other reason, and haven’t yet found a place to get into crypto — now looks like a good time to act, or to add to existing exposure if you want more…

The alert went on to describe, in significant detail, a confluence of factors that were all highly bullish for the Bitcoin space. (We didn’t know about the biggest factor of all at that time — the Tesla plan — but again, our strong hunch here is that others did.)

In the week that followed the alert, the crypto-related equity buying intensified — driven, in our view, by insider awareness of Tesla’s big reveal — and then on Friday, Feb. 5, the buyers just went wild.

By “wild,” here is what we mean: In the TradeSmith Decoder model portfolio, our largest crypto-related equity holding — and our largest stock position by far — saw a 22% gain in value on Feb. 6 alone.

Twenty-two percent in one day!

And that was on top of 700% gains in less than a year — and today (after the Tesla announcement) it is flying higher still. (We still maintain a very large position.)

At first, upon seeing Friday’s “melt-up” style close — with our other BTC-related equities having gone vertical, too — we could find no rational explanation.

But then the Tesla announcement cleared things up.

On seeing the Tesla announcement, it instantly became clear: For one of the most valuable and high-profile companies in the world to plunge headfirst into Bitcoin — and accept it for payment — is game-changing news, and folks in the know were buying crypto stocks across the board in advance.

Insider trading will never be stamped out, no matter how hard the SEC cracks down on it. It is just too lucrative under the right (or perhaps wrong) circumstances, and too many people will be tempted.

Then, too, that strange question remains: If Bitcoin is more of a commodity than a security, were laws officially broken?

Either way, here is the beautiful thing for us: Insiders can’t hide their footprints, and there is nothing illegal or nefarious in acting on those footprints.

If someone wants to buy in size based on what they know — and if they have to do it quickly, before the news is revealed — their buying footprint will show up in the price action.

And price action is, of course, completely public information. That means observant traders and investors can recognize something is afoot (no pun intended), and possibly take lucrative action on that knowledge.

That is what we did, in part, with our “Urgent Bitcoin Buy Alert” to TradeSmith Decoder subscribers Jan. 29. Though we had no advance knowledge of what Tesla was going to do, there were plenty of other confirming signals, and our strong suspicion now is that others did, in fact, know — and tipped us off via price action as they bought with both hands.

Has Bitcoin (and the Entire Crypto Space) Been Boobytrapped by Tether? No.

By: Justice Clark Litle

4 years ago | Investing Strategies

Did you dramatically increase your net worth in 2020, and book “life changing profits” while doing so?

If not, you should consider TradeSmith Decoder, because at least one of our subscribers did (and possibly many more).

We recently received a wonderful testimonial that illustrates what TradeSmith Decoder is all about: Helping people build real, life-changing wealth through the trading and investing process.

The reason TradeSmith Decoder makes that possible is because we provide real and powerful analysis (on a daily basis) along with compelling trading and investing opportunities (in real time).

It’s not about scalping for pennies or trying to catch a quick pop. TradeSmith Decoder is about big opportunities and big trends.

At any rate, the testimonial we received is below, slightly edited for clarity, and with the names of investment holdings redacted. (Because it wouldn’t be fair to our paid Decoder subscribers to give away the specific stock names.)

We are sharing the testimonial not just because we’re proud of our work — helping someone build wealth is a wonderful feeling — but also because the reader forwarded an intriguing article raising an important question about Bitcoin’s relation to Tether (a well-known U.S. Dollar stablecoin).

Read on for yourself, and then we’ll address the Tether question:

Dear Justice,

Thank you for your excellent analysis and remarkable talent for simplifying and clearly explaining complicated financial issues.

Thanks to Decoder, I invested about $190,000 in [REDACTED] and $45,000 in [REDACTED].

I had originally planned to hold my positions for the long term. Due to the information I am forwarding to you… I recently fully sold out and booked life-changing profits of just over $700,000 -— increasing my net worth over 50% in less than a year. THANK YOU!

I know you will appreciate the intellectual quality of the Tether article I am forwarding and I hope, as busy as you must be, that you will be able to analyze/comment/reply. THANK YOU!

The article’s author starts out by describing the large Bitcoin purchase he made in March 2020. (We, too, made a large Bitcoin purchase in March 2020, shortly after the panic lows, via TradeSmith Decoder — and still hold a large position.)

But the author then describes why he sold his Bitcoin position, and more or less exited crypto markets, out of concern that Tether, a popular USD stablecoin, is a counterfeit operation that is artificially inflating crypto prices across the board.

The whole article is more than 5,000 words long. We’ll try to summarize the gist as we understand it:

U.S. dollar stablecoins, or USD stablecoins for short, are crypto assets redeemable at a fixed rate of one dollar per coin or something very close to that (e.g. $0.9979). Stablecoins are useful because they let fiat dollars move freely through the crypto ecosystem.

Sometimes a crypto investor will want to cash out of a particular holding, but not necessarily turn their money back into fiat currency. In that instance, they might want to, say, exchange the crypto asset they are selling for an allotment of USD stablecoins, which are, again, like holding U.S. dollars in crypto asset form.

Many offshore exchanges cannot accept fiat currency due to outsider status relative to the banking system. These exchanges can accept USD stablecoins, however, or they can accept Bitcoin purchased through a cryptocurrency portal that also converts fiat currency (like Coinbase, Square, or PayPal).

“Crypto Anonymous,” the author of the piece, asserts that Tether’s USD stablecoin is not legitimate and above board, in the sense that it isn’t fully backed by actual U.S. dollars. There is circumstantial evidence, alongside a history of shady dealings, that suggests Tether does not have a large enough quantity of actual dollars in its accounts to redeem USDT (the Tether symbol) at a true exchange rate.

The author further asserts that USDT (Tether) is essentially a Ponzi scheme, and that many offshore exchanges — including Binance, the biggest non-U.S. crypto exchange in the world — are in on the Ponzi scheme.

The author presents evidence to suggest that real U.S. dollars enter the system through legitimate outlets like Coinbase, PayPal, and so on; that those dollars are exchanged for Bitcoin; and that the Bitcoin then migrates to other offshore exchanges, where it gets exchanged for Tethers (which are more or less a counterfeiting game).

In this manner, fake USD Stablecoins (not backed by actual dollars) are propping up Bitcoin, and supporting the entire crypto market, and the exchanges that are in on the deal are minting real profits by taking in real Bitcoin, swapping them for worthless Tethers, and then cashing out the Bitcoin for real profits via the back door.

It’s a lot to process — maybe we can summarize it further with a simple transaction chain:

1) Real dollars → BTC bought on real exchange → BTC moved to Ponzi exchange

2) BTC swapped for counterfeit Tether → Ponzi exchange cashes in BTC for real dollars

A further aspect of the scheme — as described by the author — is the habit of Tethers being handed out like candy as a way to back promotions and draw BTC into the system.

Imagine an investor with $50,000 worth of BTC held at Coinbase, who then hears about a promotion from a Ponzi exchange for a $500 sign-up bonus paid in Tether.

The investor moves $10,000 BTC over to the Ponzi exchange for the sign-up bonus, and now the Ponzi exchange can start swapping BTC for Tether (which are worthless) and earn profits through the backdoor.

The author sees this whole chain of events as risk to Bitcoin, not because Bitcoin itself has counterfeit issues — Bitcoin has never been counterfeited — but because Tether could be a significant source of activity in the crypto ecosystem.

As such, the author implies that Tether is a “doomsday machine” because, when the crypto community realizes that Tether does not have sufficient dollars to back its coin issuance, the result will be a kind of Bernie Madoff moment where faith in the crypto ecosystem collapses, causing Bitcoin’s price to plummet.

The article is very elegantly constructed. “Crypto Anonymous” makes a convincing case, and we can see why many crypto investors are deeply concerned.

In our view, though, the central argument has some fatal flaws.

One of the biggest problems is that Tether (USDT) can be readily exchanged for actual, real dollars at multiple points in the crypto ecosystem.

For example, the author acknowledges that Kraken, a sizable U.S. crypto exchange, allows for the free exchange of Tethers (USDT) for fiat dollars.

That alone is a major problem for the story. If holders of Tether can directly exchange USDT for dollars, then Tether could face a “run on the bank” in the sense that more real dollars would flow out than in.

Nor is it just Kraken where USDT can be exchanged for real dollars. There are multiple other avenues by which Tethers can be swapped out for real dollars.

Take USDC, for example, a USD stablecoin competitor with a $6.2 billion market cap.

Tether has significantly higher velocity than USDC — velocity is a measure of trading volume and rate of daily turnover — because Tether is the most popular U.S. dollar stablecoin by far.

But if the crypto space lost faith at the margins in Tether, activity and velocity could easily switch to another stablecoin competitor, like USDC or BUSD or PAX. And if any of those outlets are redeemable for real dollars, that means Tether, too, is just a few clicks away from redemption.

The point here is that the very nature of cryptocurrency — and the ease with which one dollar stablecoin can be switched with another, along with the various nodal points where Tether can be directly or indirectly swapped for real dollars — make it very hard to run a true Ponzi scheme.

Another problem with the assumption that Bitcoin relies on Tether for support — because this analysis is really about downstream liquidity effects on Bitcoin, not Tether itself — is the fact that Tether’s market cap is roughly $26 billion, whereas Bitcoin’s market cap, as of this writing, is $711 billion.

So Bitcoin’s market cap is not only 27 times larger than Tether’s, Bitcoin itself also has points of exchange all over the place where BTC can be exchanged for real dollars. That, in turn, makes it hard to argue that BTC is only being supported by Tether liquidity.

If this were true — if Bitcoin’s demand were artificially supported by Tether swaps — then BTC would be leaking out of the system via dollar sales all over the place.

Additional arguments cast doubt on the Tether argument. One would have to assume that Binance, for example — one of the largest and most innovative crypto exchanges in the world — is running a giant counterfeiting scam.

Given the operational excellence of Changpeng “CZ” Zhao, the brilliant and innovative CEO-Founder of Binance — along with all the technical accomplishments and innovations Binance has achieved — we suspect it is far more likely that Binance’s profits are real, and that Binance is making money hand over fist from a booming crypto asset space.

But if Binance’s profits are real — just as their innovation is — why in the world would they jeopardize all that for blatant participation in a seedy Tether scheme?

The Tether argument has other big problems too, like the fact that disreputable offshore exchanges are known to inflate their trading volume by an extreme degree.

If the actual trading volume on these assumed Ponzi exchanges is actually much smaller than it appears — because the also-ran exchanges inflate the numbers — that would suggest the volume of trading done to facilitate the Bitcoin-for-Tether scheme is also much smaller than it appears.

Then, too, on the positive-demand side for Bitcoin, we know that institutional hunger for BTC is a real and growing source of Bitcoin liquidity.

When we look at demand assessments from sources like PayPal, Square, or the Grayscale Investment products, we can know those flows are real; those outlets are buying Bitcoin because the underlying customer demand is real.

And we can further read the research reports and expressed statements of the institutional community — including places like JP Morgan, Fidelity, Guggenheim, Ruffer, and many others — and clearly assess a real and growing demand for BTC as a global store of value alternative.

And so, all told, we think the “Crypto Doomsday Machine” argument is elegant and persuasive — but we don’t buy the charge that Tether funny business is an existential risk to Bitcoin liquidity demand.

In fearing Tether’s impact on Bitcoin, there are too many problems with the assumption that Tether can run a Ponzi scheme easily with all kinds of instant-switch mechanisms available (just buy a different USD stablecoin, for example); with the assumption Tether is an unrivaled source of Bitcoin liquidity (there are other large-scale sources, growing larger by the day); with the assumption Binance is not playing it straight (that would be illogical, and is incongruent with their innovation track record); and with clear, empirical evidence that institutional demand for Bitcoin is high (and growing). Is Tether shady? Absolutely. We put a red flag on their accounting practices years ago.

But is Tether a source of liquidity risk for Bitcoin? All told, we are skeptical. It’s a good argument, but it doesn’t hold up.

In closing, though, we’ll make one last point. The crypto asset space may not face existential collapse risk from Tether (we just don’t see it) — but there could, in fact, be severe downside risk simply from the fact that crypto assets are white-hot right now.