We recently noted a study of six money-making market factors that date back to the year 1800.

One of those was the “value” factor, in which cheap stocks outperform expensive stocks over long periods of time.

This shows how, when it comes to financial markets, many things change, but some things stay the same. And yet, in some ways at least, the value investing landscape has radically shifted.

The Kraft Heinz share price meltdown shows how a popular version of value investing — as practiced by the most celebrated value investor of all time, Warren Buffett — has changed forever.

On Thursday, Feb. 21, the Kraft Heinz Company (Nasdaq: KHC) reported earnings. The announcement was a nightmare.

Not only did the company miss Wall Street estimates and issue weak guidance for the coming year, it slashed its dividend by more than a third and took a $15.4 billion write-down on the value of multiple flagship brands. To add insult to injury, it revealed an SEC inquiry (minor, but embarrassing) into an accounting discrepancy in one of the company’s departments.

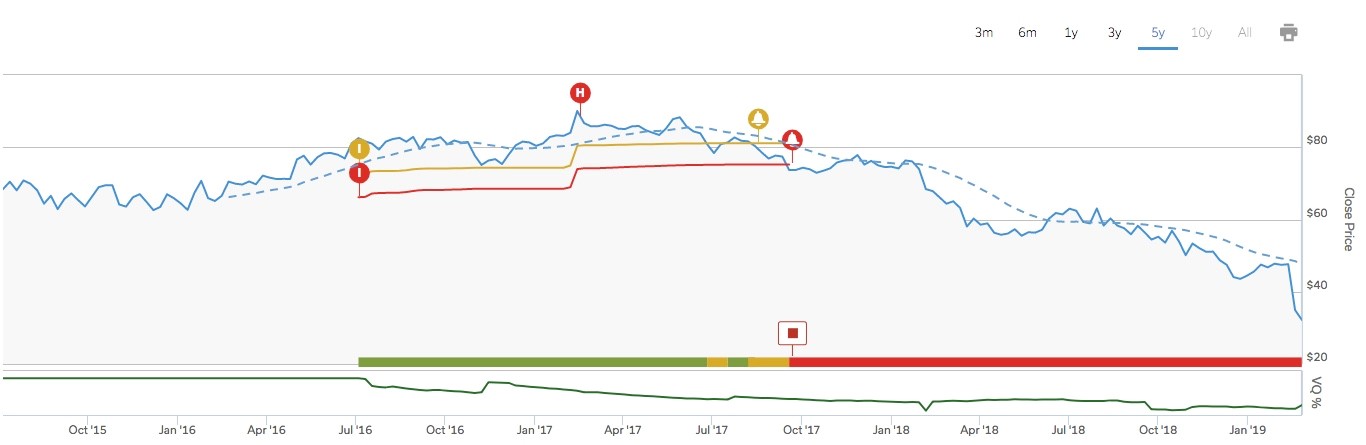

Investors reacted with horror to the Kraft Heinz report. The company’s share price, which was already at a multi-year low, fell nearly 30% on blow-out level volume. You can see the extremity of the price move in the multi-year chart below.

|

Kraft Heinz was supposed to be the ultimate value stock.

Warren Buffett’s Berkshire Hathaway teamed up with 3G, a Brazilian private equity firm, to jointly buy consumer foods company Heinz in 2013 (the famous makers of ketchup).

In 2015, they merged Heinz with Kraft — the home of Oscar Mayer and Kraft Macaroni and Cheese — in a deal that valued Kraft at $62.6 billion.

“This is my kind of transaction,” said Buffett at the time of the 2015 merger, “uniting two world-class organizations and delivering shareholder value.”

The Kraft Heinz entity went public with a market cap of $89 billion. Today, some four years later, it is worth less than half that. Berkshire Hathaway owns 27% of KHC.

“We overpaid for Kraft,” Buffett told CNBC’s Becky Quick on Feb. 25. “Anything, almost anything at a price can be good. But everything at a certain price can be bad. If you pay too much, you pay too much and that doesn’t change.”

When Kraft Heinz announced its terrible earnings reports, multiple other food and beverage companies fell in sympathy. That is partly because the problems faced by Kraft Heinz are hitting the entire industry.

For at least the past few years, if not the past decade or more, well-known food and beverage companies have seen a relentless focus on cost-cutting. The idea was to ramp up the profit margins of household brands with a ruthless focus on efficiency, slashing expenses to the bone.

This trend was led by 3G and embraced by activist hedge fund managers.

The main tool that 3G and others used was something called Zero-Based Budgeting, or ZBB for short. The idea behind ZBB is to examine every single cost, with the goal of trimming every conceivable ounce of fat. If a cost can’t be justified afresh when it comes up for annual review, the budget item is cut.

This hyper-emphasis on costs increases profit margins. Or at least it is supposed to. The problem that Kraft Heinz and other consumer goods companies ran into was that, after a while, their cost-cutting efforts made them so lean they were almost anorexic. Instead of innovating, they were stagnating.

And then consumer tastes changed, away from traditional comfort foods and more toward healthier options, with fewer preservatives and more natural ingredients.

The brand value of Kraft Heinz and other household names then started to shrink, and the trouble was made worse by the rise of private-label brands. For example: Kirkland, the in-house private brand of the giant retailer Costco, does more volume than all the Kraft brands put together.

Meanwhile the “de-branding” phenomenon is also hitting these companies. Amazon Prime customers are increasingly willing to go with whatever brand is the lowest cost, especially if the site labels it “Amazon’s choice,” and in-store private label brands are gaining ground. Trust is being transferred from the brand to the platform.

“[3G and Berkshire] both misjudged the retail versus brand fight as to who would be gaining ground on the other,” Buffett told Becky Quick. “With Amazon and Walmart fighting, it’s a bit like the elephants fighting. The mice get trampled.”

This is about more than just food companies, or the price paid on a large acquisition. A whole style of value investing, with an emphasis on milking the power of old-school brands through a combination of efficiency and inertia, is going away.

One of the co-founders of 3G, Jorge Paulo Lemann, admitted this straight out at a Milken Institute investment conference last year.

“I’m a terrified dinosaur,” Lemann said as reported by the Financial Times. “I’ve been living in this cozy world of old brands [and] big volumes. You could just focus on being very efficient and you’d be OK. All of a sudden, we are being disrupted in all ways.”

In the Berkshire Hathaway annual letter for the year 2007, Buffett explained this style of value of investing — a style he has championed for decades — as follows:

A truly great business must have an enduring “moat” that protects excellent returns on invested capital” Long-term competitive advantage in a stable industry is what we seek in a business. If that comes with rapid organic growth, great. But even without organic growth, such a business is rewarding. We will simply take the lush earnings of the business and use them to buy similar businesses elsewhere.

The trouble today is that “stable industry” is becoming an oxymoron. We are in a period of such rapid technological change that the concept of the stable industry is ceasing to exist.

Today, nearly all industries are ripe for disruption — including some whose core functions haven’t changed for decades. Think about what happened to newspapers. With self-driving cars, insurance companies could be next. With medical advances and the blockchain, health care giants are also under siege, and so on.

In short, the safe and stable are becoming the hunted and disrupted. Big, pedigreed companies with a trophy case of household brands no longer have defensible moats. They are threatened by flying drones.

The new moats are different from the old moats. They are rooted in technology and innovation and the ability to pivot, rather than customer loyalty or long-lived brand pedigree. And the new moats typically require smart investment in new technology or new products, rather than preserving the status quo.

A positive example of new moat thinking can be found in Walmart, a brick-and-mortar giant that has held up under Amazon’s onslaught.

In its latest earnings report, Walmart reported impressive results thanks to big strides in online grocery delivery. Though it is far behind Amazon in e-commerce overall, 90% of Americans live within 10 miles of a Walmart store. That has created an opportunity for Walmart to stay dominant in the grocery space.

Walmart has expanded online grocery pickup services to more than 2,100 stores, The Wall Street Journal recently reported, and offers online grocery delivery in more than 800 stores.

The key thing is that, to protect its franchise, Walmart is investing and innovating in areas of natural advantage. Instead of hanging back, it is building the future. This is what the new moats are all about.

Whereas the old moats could exploit the status quo with the help of a marketing budget, Kraft Heinz shows why that no longer works. The new moats are based on the ability to pivot and innovate at scale.

This shift has real implications for investors, and particularly for value investors. It is no longer clear what constitutes a “safe” stock and what does not, or where long-term stability can be found and where it cannot. Many longtime household names, like Kraft Heinz, are destined to become busted and disrupted “value traps” (the term for a stock that looks cheap, but then just keeps getting cheaper).

This makes it all the more important to think about the “why” behind the pricing of a value stock.

Is the company cheap for cyclical reasons that will show a turnaround? Is there some other reason to be confident in the trajectory of the business? Or is it one of the disrupted and a possible value trap?

This further adds to the value (no pun intended) of seeking to combine multiple factors when seeking out attractive investment ideas.

For example, it is possible to focus on stock ideas that represent value, momentum, and trend at the same time, by taking the following three steps:

- First, identify the area of value (based on company or industry valuation).

- Second, wait for positive momentum (bullish movement in the stock).

- Third, add to the position when a bullish trend pattern is established.

If you take all three of those steps, debacles like Kraft Heinz can be wholly avoided (our Stock State Indicator dropped into the red zone for KHC a long time ago).

|

At the same time, entry timing for attractive value stocks can be pinpointed with software (by waiting for the point at which momentum is established, then waiting again to add more in a bullish trend).

With the old moats under assault by flying drones — and the new moat candidates sometimes difficult to identify — the help of software on the investing journey can be more valuable than ever.