There are at least three broad possibilities for markets this year.

The first possibility, one that many investors fear, is that we see a global downturn, a U.S. recession (the first in more than a decade), and a bear market for stocks in 2019.

The second possibility is that markets already saw their worst in the fourth quarter of 2018 — counting as one of the quickest bear markets ever, with evidence of a “V-bottom” recovery already in place.

In this scenario, bullish forces send stocks to new all-time highs, resetting the clock on recession fears.

The third 2019 possibility, and the least likely, is the onset of full-blown financial crisis. And the potential hinge for all of these scenarios is not the United States, but China.

One of the biggest questions facing markets right now is this: Will the U.S. and China reach a trade deal?

We can lay out three scenarios based on the answer to that question.

- The resolution of U.S.-China trade tensions would be seen as quite bullish, which could inspire U.S. equities to continue on their V-bottom recovery path.

- Failure to resolve trade tensions could mean China’s economy slows even further and their real estate bubble pops, sending the global economy into recession (and possibly the U.S., too).

- The third scenario — which has the lowest odds — is China experiencing full-on economic collapse. This would be frightening and could trigger a domino chain too ugly to contemplate. Gold wins big in this scenario.

These three scenarios do not have the same probability.

The bullish outcome is the most likely. That is because, in terms of trade tensions, both Washington, D.C., and Beijing have strong incentive to come to the table.

The bearish scenario, leading to a global recession, is probably half as likely as the bullish one — we’ll call it somewhat likely. It’s the incentive thing again: The powers-that-be have strong incentive to avoid this.

And the crisis scenario, in which China experiences economic collapse, is least likely.

Factors like these explain why recessions are so hard to predict. It’s not just reading economic tea leaves. To be certain in a “recession” or “no recession” forecast, you need predetermined knowledge of how key scenarios will unfold, involving human actors and a great number of other things.

There is no definitively established economic theory as to what causes a recession. But as the economist J. Bradford Delong points out, if we look at the four U.S. recessions of the past 40 years, we can see that all of them had unique triggers.

The recession of 1979-1982 was caused by the U.S. Federal Reserve trying to “break the back of inflation” with sky-high interest rates. Beating inflation was seen as worth the economic pain, and set the stage for the major bull run that followed.

The next U.S. recession, in 1991-92, came in the aftermath of the savings and loan crisis.

Then the 2000-2002 recession came after the bursting of the dot-com bubble, and the 2008 global financial crisis followed a subprime crisis and U.S. housing bubble.

So, recessions don’t just happen out of the blue. They are typically triggered by something.

History also shows evidence of big market drops, followed by immediate recovery and new equity highs. This gives precedent for a bullish stock market scenario in 2019.

For example, in late 1998, it looked like the technology bull run had ended when Russia defaulted on its debt and the hedge fund Long-Term Capital Management famously imploded.

But the stock market recovered from those 1998 body blows, and roared again in 1999. The dot-com frenzy didn’t peak until the spring of 2000, more than 15 months later.

Here and now, it appears that, when the U.S. stock market saw its worst December since the Great Depression at the end of 2018, investors were primarily reacting to the Federal Reserve hiking rates.

The market was expressing shock and worry at the notion that Jay Powell, the new Fed Chairman, would keep hiking rates when everything appeared so vulnerable.

But then Chairman Powell expressed the verbal equivalent of “my bad” and seemed to back off, acknowledging that moving too quickly on further rate hikes could do a lot of damage.

That is why markets roared back — the Fed saying “my bad” — with one of the most extraordinary “V-bottom” type patterns markets have seen in decades. It’s visible in the S&P 500 chart as shown below.

|

Wall Street economists and investment bank research departments have a wide range of estimates as to the likelihood of a 2019 recession. Their odds range from as low as 15 percent to as high as 64 percent.

Rather than play an impossible guessing game, though, we would say watch what happens with China.

The V-bottom pattern, which is present in crude oil as well as the major U.S. indexes, suggests that investors remain optimistic even with the global economy looking shaky.

But a China deal will have to go through for that optimism to be justified.

The odds of a China deal are the most likely of our three scenarios because both sides are strongly incentivized to make a deal happen.

In Washington, the Republican-led executive branch is starting to think about the 2020 elections. They want a happy, healthy stock market if at all possible — not a bear market right beforehand — and a trade deal with China is a significant piece of keeping markets happy.

In China, meanwhile, the leadership in Beijing knows the economy is in trouble.

An estimated 1 out of 5 apartments in China (65 million in total) are unoccupied; there are longstanding fears of a popping real estate bubble; and the Shanghai Composite was already one of the worst performing global indexes with a more than 30% peak-to-trough decline in 2018 (see chart below).

|

At the same time, China is sitting on mountains of bad loans — as much as $8.5 trillion by some estimates — and capital is leaving the country. Xi Jinping, China’s leader-for-life, cannot afford the economic pain of an ongoing trade war right now and he knows it.

The win-win for Washington and Beijing would be a new trade deal where China agrees to a big, impressive headline number for purchasing U.S. goods — say $1 trillion or more over a period of years — while the more thorny issues of intellectual property theft and currency manipulation get back burnered.

A headline deal of that sort would be greeted with major enthusiasm by investors. The White House would be able to tout a major win. China’s leadership would endure some short-term pain, but see gain in the ability to keep playing the “long game” while avoiding harsher intellectual property penalties.

If you put together a Washington-China trade deal, a gaudy headline, and a Federal Reserve that is committed to backing off, it is easy to see how investors could ramp up optimism again — as they did in 1999, after the 1998 scare of the Russian debt default and Long-Term Capital Management blow-up.

Again, a bullish deal is the most likely scenario given the incentives. But it’s always possible for things to go wrong, and for trade negotiations to go south for whatever unexpected reason. The deeper issues causing tension between the U.S. and China are also very real, and hard to sweep under the rug.

That a “no deal” scenario, in which China continues to struggle under the weight of US trade tariffs and their pain gets even worse, is somewhat likely.

This would be bad news for the global economy — China imports more than $2 trillion per year worth of goods — and a big drag on U.S. corporate profits, with roughly half of S&P 500 profits earned overseas. (The U.S. information technology sector has the highest foreign exposure at close to 57%.)

With a “no deal” result, it’s easy to see how investor worries intensify as corporate profits get hit.

This could lead to a psychology shift towards pessimism, worsened by many other problems the world is facing right now, and a resumption of the flash-in-the-pan bear market that hit markets hard in Q4 2018.

The last possibility, and the one with the lowest odds, is China seeing a full-on economic collapse.

Hawkish China watchers have been predicting a collapse for many years, due to China’s unsustainable rate of state-run investment, questionable or even phony economic statistics, and an alarming mountain of debt.

There are very smart analysts who believe China’s economy is the equivalent of a giant Enron. Other smart analysts strongly disagree, but the “China as Enron” case has sobering evidence behind it.

A macro crisis out of China is the kind of thing for which the timing can’t be predicted.

But the longer the unsustainable debt levels pile up the more likely it becomes, and a U.S.-China trade war escalation — in which not only is there “no deal,” but the U.S. ratchets up the tariff pressure and economic isolation further — could finally cause the China crisis dam to break wide open.

If a macro crisis bursts forth out of China, all bets are off as to what happens next to stocks and the global economy. Although some of the scenarios are very, very bad (like Beijing talking up an invasion of Taiwan, for example, to distract from civil unrest as the Chinese populace revolts).

Again though, a China collapse is the low odds scenario for 2019.

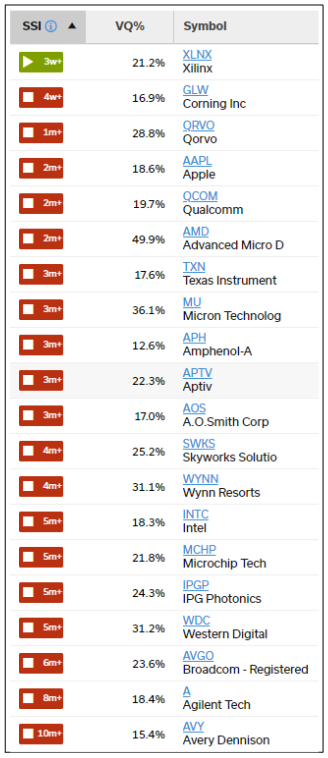

Goldman Sachs has put together a list of publicly traded U.S. companies with a high percentage of revenue exposure to China. That exposure could be a good thing or a bad thing, depending on investor sentiment and U.S.-China trade deal prospects.

You can see the SSI ratings for these companies below, and follow the list as a kind of bellwether tracker for the China outlook.

|

Most of these China exposure names are in the red right now. But if a banner headline comes through on a breakthrough in China trade talks, that could change.

Either way, keep an eye on U.S.-China trade tensions, and their possible resolution, as a key driver for whether the stock market turns bull or bear in 2019.