Many retirees have a vague sense they could achieve significantly better returns managing their investments themselves.

Yet, they hesitate. Often, that’s because managing a portfolio sounds complicated.

And of course, the big brokerage firms want us to feel overwhelmed.

They’re quick to show us studies that “prove” how individual investors can’t outperform the markets.

Today, I’d like to tell you a story that shows how you can not only outperform the markets—I’m going to show you two easily available resources that can help you capture gains that will embarrass your broker!

Recently, a colleague of mine asked me to take a look at his mother’s portfolio.

She’s 72 and for the past 8 years, she’s trusted one of the large brokerage firms to manage her investments. (We’re withholding the firm’s name to protect the guilty.)

Our heroine’s investments were placed in one of the firm’s many cookie-cutter “portfolio solutions” products—a service for which she pays nearly 2% per year.

Her fees are far from trivial, something I’m sure you’ll fully appreciate after you see what she received for her money.

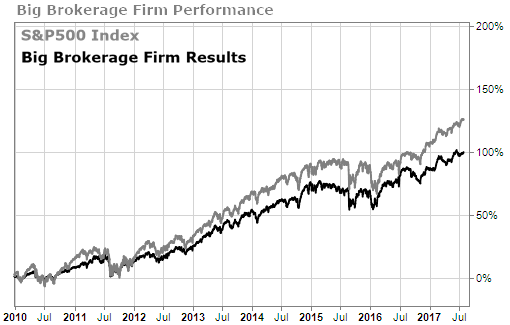

The stocks her brokerage firm has her in are all well-known, blue-chip companies like IBM, AT&T, and Walmart. As a rule, they pay regular dividends.

From 2010 through August of this year, she’s seen gains of close to 100% in her account—a fact her broker has no doubt reminded her of.

Yet, in the greatest bull market of this century, she was severely underperforming the S&P 500!

It would be one thing if she were invested in a mix of stocks and bonds, but 100% of her investments were in stocks. And she was close to 100% invested at all times.

When my colleague, who works for a well-respected stock-advisory, glanced at his mother’s portfolio, he saw right away that her gain didn’t stack up to what the S&P had done over the same span of time.

He asked me if I’d have a look and I agreed he was right on the money with his assessment.

Have a look and see for yourself…

Back in 2010 Mom’s original investment in her IRA was in the neighborhood of $91,000. In August of 2017, her portfolio was worth $168,000.

Keep in mind, at 72, she’s also taking her annual Required Minimum Distribution (RMD). Over the past 3 years, that adds up to close to $18,000.

Total fees to the brokerage firm?

$14,658, or 15% of the gains she’s made.

I’d call that a pretty hefty premium, paying someone 15% of your profits to underperform the S&P—something the brokerage firm likely forgot to mention.

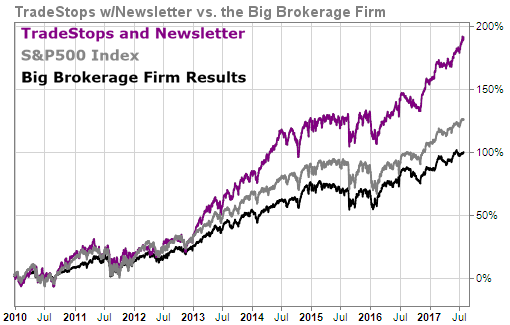

Especially when you consider there’s a much better alternative. One that doesn’t cost nearly as much and provides vastly superior returns.

With her permission, I showed her how using nothing more than suggestions from a popular newsletter and the tools inside TradeStops, could have almost doubled her returns!

Of course, TradeStops isn’t free. Neither is the newsletter subscription.

The good news? Those costs are figured into the above analysis.

We deducted the amount of the current price of TradeStops from the original 2010 portfolio value. We also factored in an annual TradeStops maintenance fee. And we included a $100 per year newsletter subscription.

So, for a one-time Lifetime TradeStops subscription (a fraction of what she paid her brokerage firm) and about $500 for annual maintenance and her newsletter subscription, this investor could have easily achieved returns that would have embarrassed the heck out of her brokerage firm.

Assuming they have any shame.