Here is a finding that will bake your noodle: Interest rates have been falling for 700 years. From the early 1300s onward, the long-term trend of interest rates has been lower.

If the data supporting this finding is correct, we are talking about one of the biggest trends in history: Bigger than any nation or human migration pattern; bigger than central banking; bigger than all wars and treaties; bigger than the industrial revolution.

The implications are staggering. For example, it is possible that a long-term interest rate decline is baked into the structural nature of credit and lending, and thus into the fabric of financial capitalism itself.

Then, too, the pattern shows we have even less idea of what the future holds than many people assumed. A trend this big could just keep grinding on for centuries more — or reverse for a decade or two, and then reassert itself.

The data comes from Staff Working Paper No. 845, published by the Bank of England (BOE), with the official title “Eight centuries of global real interest rates, R-G, and the ‘supersecular’ decline, 2011-2018.” You can read it via PDF here.

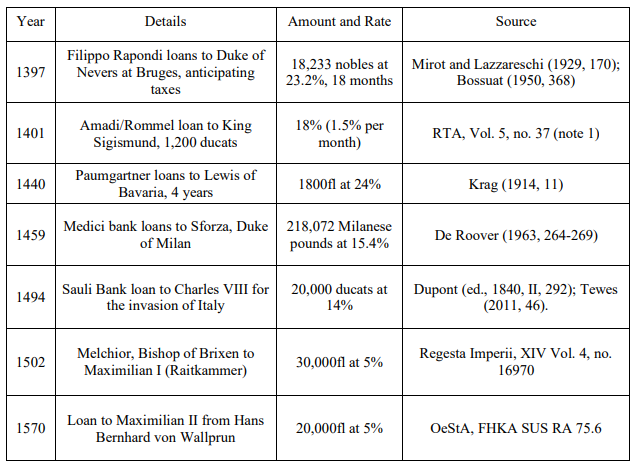

In the paper, BOE researcher Paul Schmelzing looks at credit and lending data going back to the late 1300s. Here is a sample of the type of data he collected:

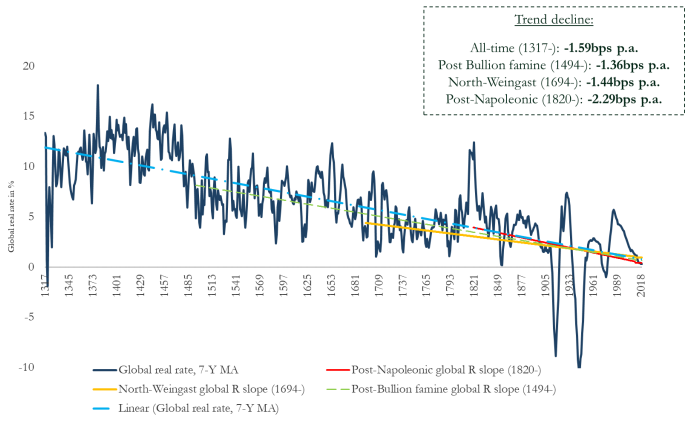

Below is a chart depicting the “global real rate,” adjusted for various factors, dating all the way back to the year 1317. When you smooth out the spikes and the noise, the average result is a decline of 1.59 basis points per year — for 700 years and counting.

As a side note, the phrase “real rate” refers to the rate of interest after inflation is taken into account.

To briefly explain, interest rates and bond yields can be thought of in two forms, the nominal rate and the real rate. The “nominal” interest rate is the published number you see in the paper. The “real” rate subtracts the rate of inflation from the nominal rate.

For example: If the nominal interest rate is five percent, and the current inflation rate is seven percent, the “real” rate is negative two percent, because five minus seven is negative two.

The real rate is what matters because, if you don’t know the inflation context, the nominal rate doesn’t mean anything. For instance, is a four percent interest rate high or low? That depends on where inflation is. If inflation is at two percent, four percent is high. If inflation is at eight percent, four percent is low. You need the “real” rate — the nominal rate adjusted for inflation — to get a sense of what matters.

The paper serves up a stunning — and highly controversial — conclusion. In Schmelzing’s own words:

Against their long‑term context, currently depressed sovereign real rates are in fact converging ‘back to historical trend’ — a trend that makes narratives about a ‘secular stagnation’ environment entirely misleading, and suggests that — irrespective of particular monetary and fiscal responses — real rates could soon enter permanently negative territory.

That is an amazing statement: “Real rates could soon enter permanently negative territory.”

But getting back to the possibility of real rates in “permanently negative territory:” If that hypothesis is correct, or anywhere close to correct, the world could be sailing into completely uncharted waters.

Pot Fortunes of More Than 1,000% in 12 Months?

After months of in-the-field testing, Matt Badiali is sharing his most dynamic investment strategy. And he guarantees that anyone who follows his recommendations will have the chance to see gains of 1,000% or more on pot stocks over the next 12 months.

As of January 2020, there is about $11 trillion worth of negative-yield sovereign debt in the world. That total has ebbed and flowed, pushing above $17 trillion at one point.

Most observers assumed that negative-yielding sovereign debt was a bizarre side effect of the 2008 global financial crisis, or rather, the emergency measures taken by central banks to fight the crisis.

This further led to the assumption that, if negative-yielding debt is an aberration, it must go away at some point. But if Paul Schemlzing is right, maybe it doesn’t.

And Schmelzing, as we know, is not some crank ginning up a wild theory on flimsy evidence: He is a researcher at one of the most respected central banks in the world (the BOE), with 700 years’ worth of data to support his conclusions.

It’s possible the global financial world has entered its own version of the Netflix show Stranger Things. Perhaps we are headed into the “Upside Down” with no way out.

There are many explanations for why Schmelzing could be correct, and why interest rates could be headed to permanently strange places. The theories involve human nature, the nature of lending and credit, Darwinist behavior patterns (strong versus weak), power structures, and much more.

There are also plenty of reasons why Schmelzing could be wrong — or wrong for the next decade or two, which would effectively be the same thing. Ten years from now, the interest rate world could look like the early 1970s, with rates approaching double digits — and the dollar dethroned as the world’s reserve currency.

The key takeaway is to stay humble and nimble, and beware of anyone who delivers a future forecast with long-term certainty. There are so many unknowns — and so many wild possibilities ahead — that staying open-minded and flexible is the only rational path for investors now.

TradeSmith Research Team